Lessons in International Small Cap

Since the turn of the 20th century, the United States has been a powerhouse when it comes to economic production. Gross Domestic Product (GDP) is a commonly used statistic to broadly measure economic production. As of 12/31/2018, the U.S. economy accounted for 24.4% of the world’s GDP – giving it the largest economic footprint of any individual country. However, in 1960 the U.S. economy held a 39.6% share of the world’s GDP. Of course, the U.S. economy is not shrinking (in fact, it has grown almost 3500% since 1960). Rather, some international economies have been growing at a faster rate. As investors, there are two ways we can reap the benefits of a rapidly developing world economy: we can simply diversify across international stocks, and, if the premium for investing in small company stocks holds overseas, we should include an allocation to international small cap stocks.

Many investors follow the S&P 500 – which actually holds 505 companies – as a proxy for how stocks are doing. These companies are all based in the U.S. and are generally large cap. The MSCI EAFE Small Cap Index, one of the more popular indices utilized in tracking the broad performance of international small cap stocks, is currently comprised of 2,355 companies across 21 developed countries. We believe the opportunity set in international small cap is enormous!

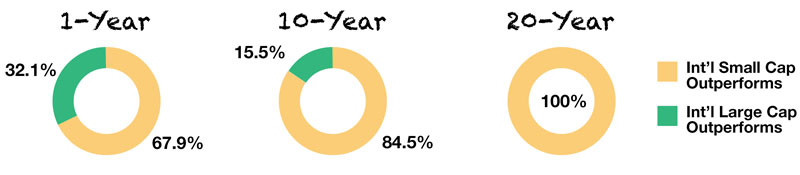

Perhaps more exciting than diversifying across a broader opportunity set, the oft-discussed small cap premium applies internationally as well! Whether at home or abroad, the reasoning goes that smaller companies tend to be riskier than larger companies, so investors must be paid with additional expected return in order to invest in small companies. From 1970 through last quarter end, international large cap stocks have returned an annualized 8.5%, while international small cap returned an annualized 13.5%. Of course, this does not guarantee that international small cap stocks post a higher return than their large cap counterparts every single year. The evidence in Exhibit 1 shows that while international small cap stocks usually post higher returns over one-year periods, the longer an individual invests in international small cap stocks, the greater the odds of outperforming international large cap.

Exhibit 1: Periods of Outperformance: International Small Cap vs. International Large Cap

Source: Morningstar Direct. Indices used: MSCI EAFE NR USD and Dimensional International Small Cap Index (1/1/1970 – 3/2019)

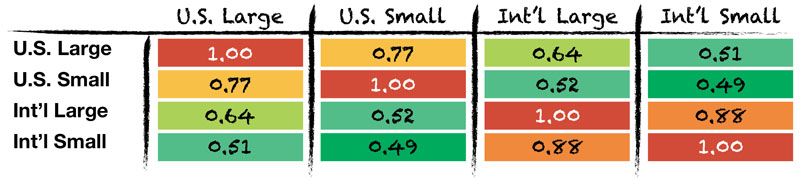

Lastly, incorporating assets with imperfect correlations can help boost the diversification benefits of a portfolio. Correlation is a statistic that ranges from -1 to +1 and is used to describe how two assets tend to move in relation to each other. A correlation of +1 represents two assets that move in lockstep with each other, while a correlation of -1 would demonstrate two assets moving in opposite directions. Examining the historical data in Exhibit 2, international small cap stocks have had a correlation of approximately 0.50 to U.S. large cap stocks since 1970. This would imply that while U.S. large stocks and international small stocks sometimes move in the same direction, they also act differently at times. When these asset classes act differently in the same portfolio, they create diversification benefits – mitigating risk and potentially increasing return.

Exhibit 2: Correlation Matrix

Source: Morningstar Direct. Indices used: MSCI EAFE NR USD, Dimensional International Small Cap Index, IA SBBI US Large Stock TR, and IA SBBI US Small Stock TR (1/1970 – 3/2019)

Takeaway: Lessons in International Small Cap

With all of these benefits to long-term investors in mind, Savant has maintained an allocation to international small cap stocks since 1993.

Sources: Morningstar, S&P Dow Jones Indices, MSCI Inc., and World Bank

Savant Capital Management is a Registered Investment Advisor. This information is not intended as personalized investment advice. Past performance is no guarantee of future results. The index returns herein assume reinvestment of all dividends and interest and do not reflect fees or expenses. Index portfolios reflected in this publication are not representative of any actual client returns. Savant’s marketing material should not be construed by any existing or prospective client as a guarantee that they will experience a certain level of results if they engage the advisor’s services.