How the Premium Tax Credit Can Help You Save on Health Care Costs

Determining whether you qualify for the Premium Tax Credit may seem daunting. Wealth Strategy Associate Abigail Ogden reviews the eligibility requirements and mechanics of how these credits work.

Premium Tax Credit Eligibility

The Patient Protection and Affordable Care Act gives eligible consumers the opportunity to purchase private health coverage through state and federal marketplaces through a convenient exchange. Subsidies in the form of tax credits were established to aid with the cost of premiums for middle class individuals and households. The marketplace and insurance tax credits can also provide a more affordable health care option for those retiring before they become eligible for Medicare.

In terms of the Health Insurance Marketplace, a household is defined as a tax-filer, spouse, and their tax dependents.

These tax credits are refundable and advanceable, but can only be claimed if the household:

- Has an income level that falls between 100 and 400 percent of the Federal Poverty Level. The 2019 poverty guidelines which guide eligibility for 2020 coverage include:

- One individual: Household income from $12,490 up to $49,960

- Family of Two: Household income from $16,910 up to $67,640

- Family of Four: Household income from $25,750 up to $103,000

- Has no eligibility for adequate and affordable health insurance from other sources.

- Has no eligibility for coverage through a Government Plan (i.e. Medicaid, Medicare, CHIP, or TRICARE).

- Is legally a United States resident.

- Does not use the “Married Filing Separately” filing status, unless a victim of domestic abuse and/or spousal abandonment.

- Cannot be claimed as a dependent by another person.

- Is enrolled in coverage through the Health Insurance Marketplace. (Though health insurance can be purchased through other sources, this is the only way to qualify for a premium tax credit.)

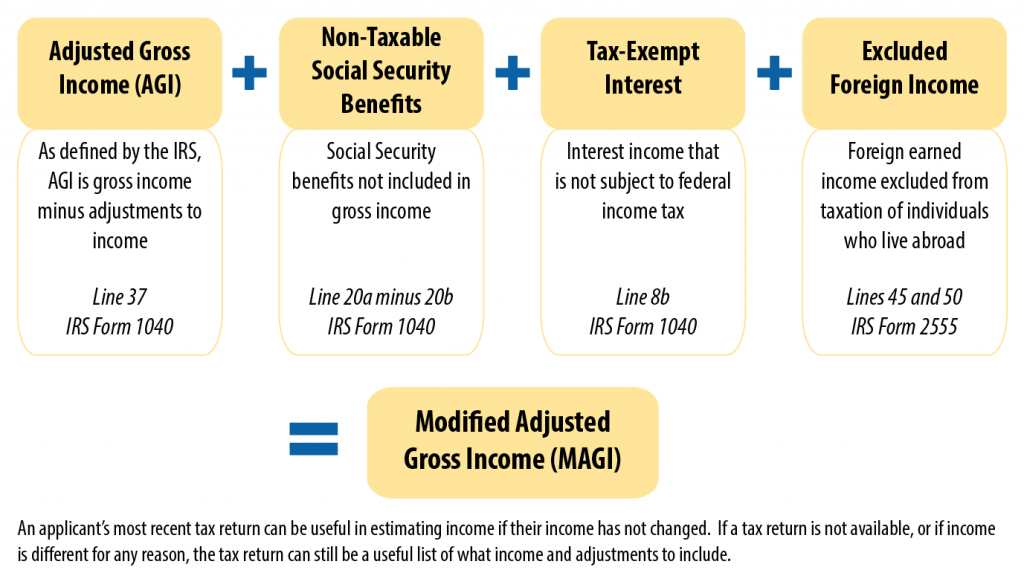

A household’s Modified Adjusted Gross Income (MAGI) is the income figure that is used to determine eligibility. MAGI is equal to your Adjusted Gross Income (AGI) plus non-taxable Social Security benefits, tax-exempt interest and untaxed foreign income, if applicable.

What is Modified Adjusted Gross Income (MAGI)?

How the Premium Tax Credit Works

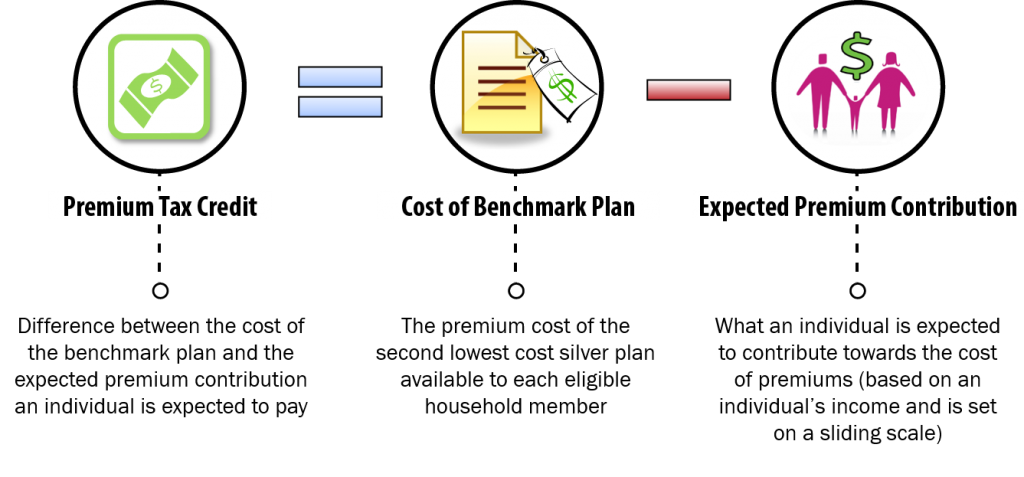

The Premium Tax Credit (PTC) is calculated by first, identifying the second-lowest cost Silver plan that is available to the household members; this is referred to as the “benchmark plan.” Next, the household’s income level is taken into consideration. The individual or family is expected to contribute a certain amount of premium, which is based on a sliding scale, to their coverage.

For example: In 2020, a family of four with an annual income level of $77,250, which equals 300 percent of the 2019 poverty line, is expected to contribute 9.86% of their income (about $619 per month) toward premium. Whereas, a family of four with an annual income level of $38,625, which equals 150 percent of the 2019 poverty line, is only expected to contribute 4.15% of their income (about $135 per month) toward the premium.

Using this information, the PTC is generally the difference between the annual cost of the identified benchmark plan and the expected annual premium contribution for each household.

Calculation of the Premium Tax Credit

What’s the difference between the Premium Tax Credit (PTC) and the Advance Premium Tax Credit (APTC)?

The Premium Tax Credit (PTC) is structured in a more retrospective manner. When filing taxes for the previous year, the tax filer’s PTC is calculated and applied to that year’s tax return, if applicable, to “pay back” the taxpayer for the portion of premium that can be covered by the credit. Because this credit is “refundable,” it is applied to the taxpayer’s liability and can either result in a refund or can be used to reduce income tax liability when taxes are filed.

An alternative, the Advance Premium Tax Credit (APTC), is more forward-looking and helps taxpayers pay for their upcoming premium. The APTC is calculated when an individual applies for coverage, and the government sends the credit amount directly to the taxpayer’s health insurance company to provide a “discount” on their monthly premium payments.

While this option sounds more appealing to most people, it is important to note that the APTC is based on a predicted/projected amount of the taxpayer’s income. Because no one can predict the future, this route tends to be more risky.

- If the taxpayer has higher income than anticipated throughout the year, including investment earnings, they most likely will receive a greater tax credit than they were eligible for. The taxpayer must then pay back the difference when they file their tax return.

- On the other hand, if the taxpayer’s income was less than projected at the start of the year, they most likely will receive less of the credit than they would have qualified for. This could result in refundable credit, like the PTC, to “pay back” the difference when the taxpayer files their return.

The Premium Tax Credit in Action

Determining whether you qualify for the Premium Tax Credit can seem a little daunting because of the many complexities and considerations that come with it. If you are retired prior to Medicare, it is important to carefully manage your taxable income from retirement account withdrawals, dividends, and interest, as well as coordinate with tax planning strategies such as Roth conversions.

If you’d like to check your eligibility or learn more about saving money on health care, visit healthcare.gov/lower-costs/ for additional information.

If you have questions regarding the qualifications or implementation of the Premium Tax Credit, or need assistance in determining what may be best for you, consider reaching out to your tax professional.

Sources: https://www.taxpolicycenter.org/briefing-book/what-are-premium-tax-credits; https://www.irs.gov/affordable-care-act/individuals-and-families/the-premium-tax-credit-the-basics; https://www.healthcare.gov/glossary/premium-tax-credit/; https://www.investopedia.com/terms/a/advanced-premium-tax-credit.asp; https://www.healthreformbeyondthebasics.org/premium-tax-credits-answers-to-frequently-asked-questions/; https://www.healthcare.gov/income-and-household-information/household-size/; https://marketplace.cms.gov/technical-assistance-resources/aptc-csr-basics.pdf