Uncle Sam: Your Partner in Retirement

Like it or not, you and Uncle Sam will be working closely together during retirement. Taxes, Social Security, Medicare, your Retirement Accounts – he has a say in all of it. Learning the rules to the game is key if you want to maximize the value of every opportunity and avoid costly missteps.

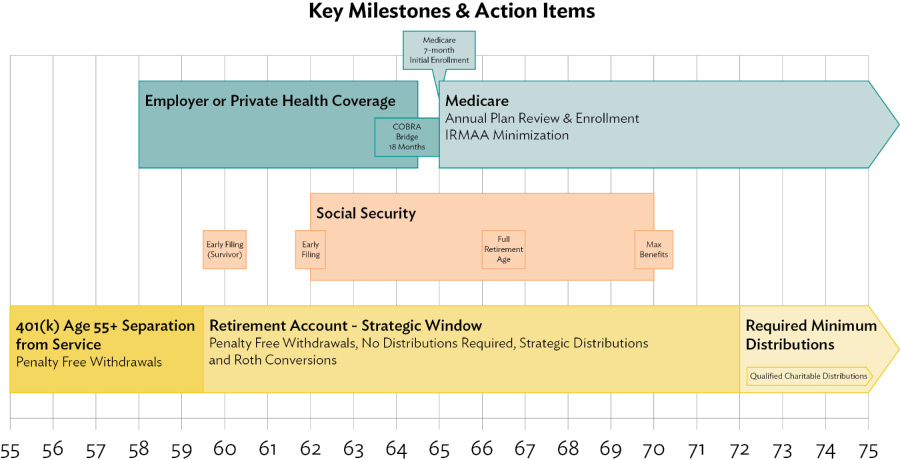

There are numerous rules, elections, and key dates in your partnership. It can be very difficult to keep all of them straight. The following graphic can serve as a handy reference to clearly plot them out for you. We’ll examine each in detail.

Retirement Milestones

Retirement Accounts

Most Americans have an IRA and 401(k) account that they use to save for retirement while also reducing their tax burden along the way. Starting at age 59½, you’re allowed to take penalty-free withdrawals from your retirement accounts. But remember, penalty-free does not mean tax-free, distributions will be included in your taxable income. Once you can take penalty-free distributions, it might make sense to make flexible distributions to satisfy your cash flow needs.

In special circumstances, you can take money out of a 401(k) penalty-free as early as 55. To do this, you must separate from service with your employer after age 55 and leave your 401(k) in place with that employer. You will still need to wait until 59½ to take penalty-free distributions from your other retirement accounts.

It may be worthwhile to consider funding or converting to a Roth IRA, which offers tax-free growth potential and tax-free withdrawals for you and your heirs, (if certain requirements are met). Instead of the traditional retirement account model where you deduct the income now, and pay tax on it later, the Roth is funded with after-tax dollars and is then tax-free going forward. We’ll talk more about the Roth vs. Traditional decision in the “Taxes” section.

When you reach age 72, you’re required to withdraw a certain amount of money from your retirement accounts each year. That amount is called a Required Minimum Distribution or RMD. It is calculated as a percentage of assets based on your age. The first distribution at age 72 will be about 3.91% of the prior year-end account balance, and the required distribution percentage will increase each year.

If you’re charitably inclined, a qualified charitable distribution or QCD, a direct transfer of funds from your IRA custodian to a qualified charity, may be an attractive alternative to taking an RMD. These distributions can count toward satisfying your RMD for the year if you satisfy certain rules. Instead of receiving an itemized deduction like you would with an ordinary charitable contribution, the QCD is completely excluded from your income. This means you don’t have to itemize to benefit from the donation and the exclusion from income might also reduce other taxes like the Medicare Net Investment Income tax and IRMMA adjustments.

Social Security

Several factors play into the decisions of when to claim Social Security including life expectancy, other sources of income, retirement age, spousal benefits, and survivor benefits.

Social Security planning is critical in virtually all retirement plans because total lifetime benefits can amount to a six- or seven-figure sum. Given that importance, people need to avoid making an emotional decision or one based on simple rules of thumb.

Many times, people focus on a breakeven date, but it’s more complicated than that. One of the things Social Security provides is a hedge against the probability that you and/or your spouse live a long time, it’s not just a math equation. On top of that, if you’ve been married, are currently married, or considering marriage, it’s not just a single life decision. There are really two life expectancies and you’ll need to sort out that dynamic. You may have a situation where the older spouse is in poor health and there’s a desire to claim early. It may make more sense to defer claiming Social Security and max out spousal benefits and survivor benefits for the younger spouse.

When we look at the statistics there are three ages that the majority of Social Security benefit claims happen – at age 62, at age 65, and at retirement. There’s nothing strategic about those points in time. To make the most of your benefits, you’ll need to think more strategically. Think about Social Security in conjunction with your spouse and the rest of your financial life.

Full retirement age, or FRA, is the age when you are entitled to 100 percent of your Social Security benefits, which are determined by your lifetime earnings. You can file as early as 62, but FRA is usually between 66 and 67. Social Security benefits generally max out at age 70.

If you defer your claim beyond FRA, benefits will increase by about 8% per year. This can provide a big boost to your long-term retirement cash flow. Claiming benefits before FRA will reduce them by 6-7% per year. Both the reduction and increases will impact your benefit for the remainder of your lifetime.

Married couples will be entitled to spousal benefits. You are not able to claim both a spousal benefit and your own retirement benefit, your benefit will essentially be the higher of the two. A spousal benefit is based on 50% of your spouse’s FRA benefit, and can be reduced further if you claim prior to your own FRA. Deferring spousal benefits beyond FRA will not provide any further benefit increases.

Divorcees can claim ex-spousal benefits if the marriage lasted at least 10 years, they are at least age 62, and remain unmarried. Your ex-spouse is not impacted in any way by that claim.

If your spouse (or ex-spouse of 10+ years) has passed away, you will be entitled to survivor benefits. This blog provides additional insights into this complex topic.

Medicare

Enrollment begins three months before the month of your 65th birthday and ends three months after. It is critical to evaluate your initial enrollment decision, as there may be penalties and lifetime consequences if you do not enroll properly. Consult with a reputable and recommended agent. Their commissions are typically built into premiums whether or not you use an agent, so it is no added cost to you. If you are still working at age 65, it is critical to coordinate your initial Medicare enrollment with your employer-provided health care. If you retire before age 65, consider your options for building a bridge to Medicare using private insurance, an ACA plan, or COBRA.

Medicare contains multiple components, or parts.

- Part A: Hospitalization coverage ($0 premiums)

- Part B: Medical coverage ($170.10 monthly premium in 2022 + IRMAA)

- Part D: Prescription coverage (premium varies, $43 national average)

Participants in Parts A & B can round out their coverage with one of the below options:

- Medicare Advantage Plan: Sometimes referred to as “Part C.” Typically $0 premium with a regional HMO or PPO network. Part D may be included with no additional premium.

- Medicare Supplement Plan: Additional monthly premiums required. Accepted anywhere in the country that accepts Medicare. Part D is not included.

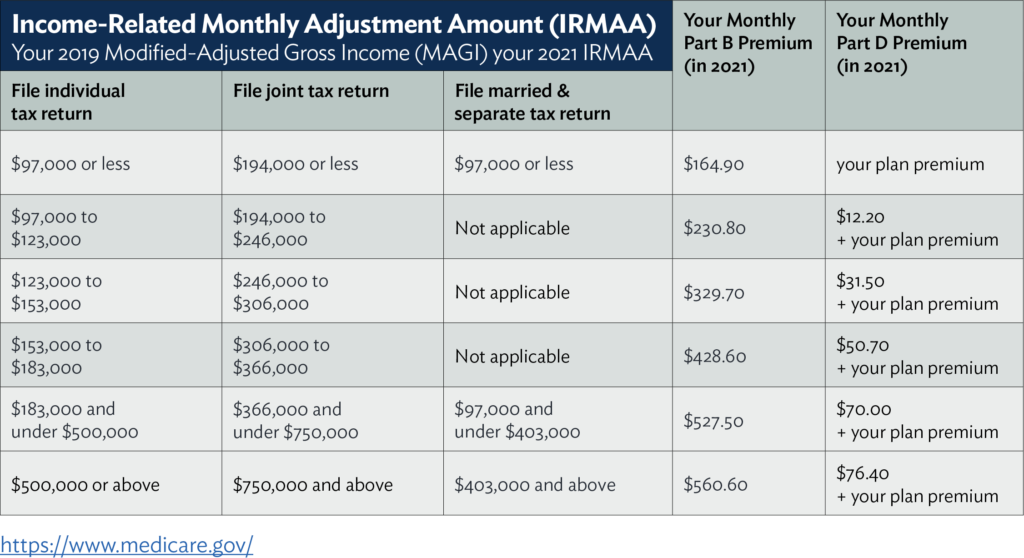

Your Medicare Parts B and D premiums are subject to increases called Income-Related Monthly Adjustment Amounts (IRMAA). As you cross certain income thresholds, you will see your Medicare premiums increase. Because these increases are not phased in, going just $1 over a threshold could increase your premium by thousands of dollars per year. Pay careful attention each year to your Modified Adjusted Gross Income (MAGI), from which the IRMAA calculation is based. Your income from your tax return two years prior will generally be the figure referenced for your IRMAA calculation.

Taxes

When it comes to paying taxes and saving for retirement, you can either pay now or pay later. The important thing is to keep a long-term focus on your taxes. It’s not just about the bottom line on this year’s tax return, but the cumulative amount over several years.

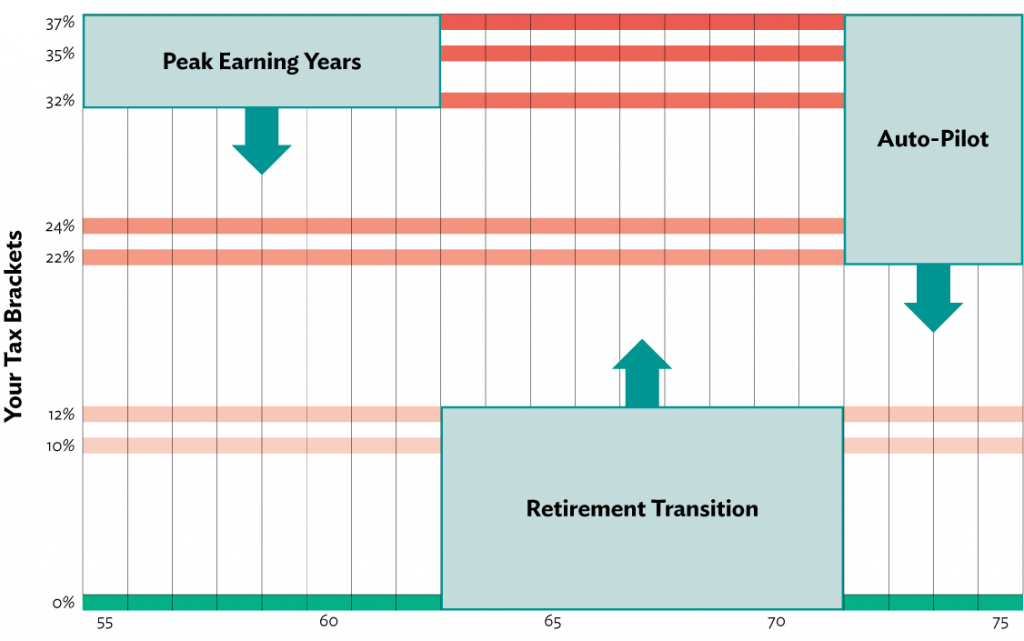

Many people worry about healthcare expenses in retirement but taxes could become your largest expense if you don’t have a strategy for managing them. The most fundamental strategy is to minimize lifetime taxes by looking for high points, low points and the equilibrium.

In the illustration above, you’ll notice that there are four tax zones — High, Medium, Low, and Zero. Along your retirement timeline there are three typical phases – peak, transition, and auto-pilot. Forecasting your income and assets into the future can help to estimate what tax zones you’ll encounter in the various stages of retirement. Determining your long-term auto-pilot tax zone will help you to make informed decisions about tax strategy in the preceding years.

In relatively high tax-bracket years, you’ll want to focus on maxing out your deductions and deferrals to lower your income. Traditional retirement accounts and deferred compensation are the primary mechanism for deferring income. Large deductions, like charity, are also most valuable to you in these high-bracket years.

In relatively low tax-bracket years, you can increase your recognition of income through Roth conversions, IRA distributions, and gain harvesting. You’ll want to forecast your auto-pilot rates and fill up any brackets below that level. Deferring Social Security during the retirement transition can have the added benefit of freeing up even more space for strategic income recognition prior to age 70. If you would like to learn more, here are five Tax-Smart Retirement strategies to consider.

Justin D. Smith

Financial Advisor

CAP®, CFA®, CFP®

Justin D. Smith

Financial Advisor

CAP®, CFA®, CFP®