Silver Linings Playbook

“An optimist stays up until midnight to see the New Year in. A pessimist stays up to make sure the old year leaves.”

—William E. Vaughan

Suffice it to say that while I did not stay up until Midnight this past New Year’s Eve, my guess would be that most who did were waving goodbye to 2022 rather than hello to 2023.

It was very easy to be a pessimist last year, surrounded by a sea of negativity in the economy and markets.

With both stocks and bonds finishing the year down in the double digits, it’s no surprise that people have gravitated towards crystal ball prognostications, investment punditry, and market playbooks as the Gregorian calendar begins anew.

We’ve all made New Year’s resolutions at one point or another – joining a gym, starting a new diet, abstaining from alcohol for Dry January, improving our relationships, or even learning a new skill or hobby.

But it turns out the whole notion of “new year, new me” can often extend beyond our personal lives and into our portfolios. This mindset may cause investors to act as though the slate has been wiped clean and that a new playbook is required. But the reality is that the clock striking midnight on New Year’s Eve doesn’t make the crystal ball any less cloudy than it was before.

Regardless, the months of December and January are “prediction season” in the investment industry. Throughout this period, the email inboxes of financial advisors become littered with the annual investment outlooks from just about every big bank, brokerage, and fund company.

I’d be lying if I said I never read or skimmed any of them. Occasionally you stumble upon a decent insight, a cool chart, or an interesting data nugget. But by and large, these publications are rarely actionable. It’s entertainment and should be treated as such.

One such outlook I encountered this year had the title of “Keep It Simple” right on the cover page.

The entire piece clocked in at 76 pages.

I guess not everyone has the same definition of simple. Go figure.

These market playbooks can make for compelling reading. But they can also make for terrible distractions to the business of investing. It’s important we distinguish between what’s interesting and what’s actionable. The former is rarely the latter.

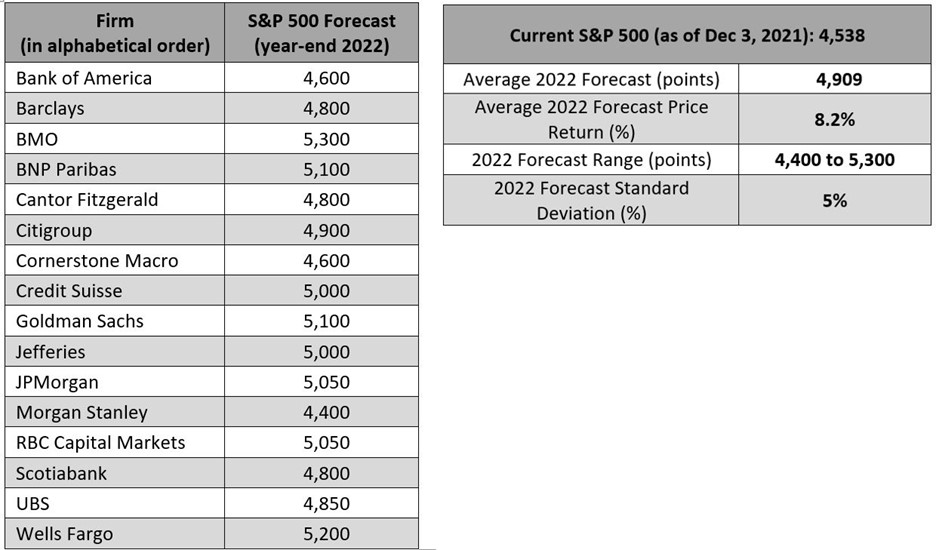

Speaking of distractions, another big distraction that gets attention every year are the year-end S&P 500 price targets. Every year they come in via the strategists at the big banks and research shops. And every year they are comically wrong. Below is a list from Janus Henderson of the year-end S&P 500 forecasts made at the end of 2021. In other words, these were predictions of where the market would finish 2022.

Source: Janus Henderson

For those keeping score, the S&P 500 finished 2022 at 3,839.50. Not a single forecast even had a 3-handle on it!

What’s not surprising is that the average of all these forecasts, in percentage terms, was about an 8% gain – within spitting distance of long-term average stock market performance. It’s quite remarkable, considering the number of man-hours and resources that go into crafting these predictions.

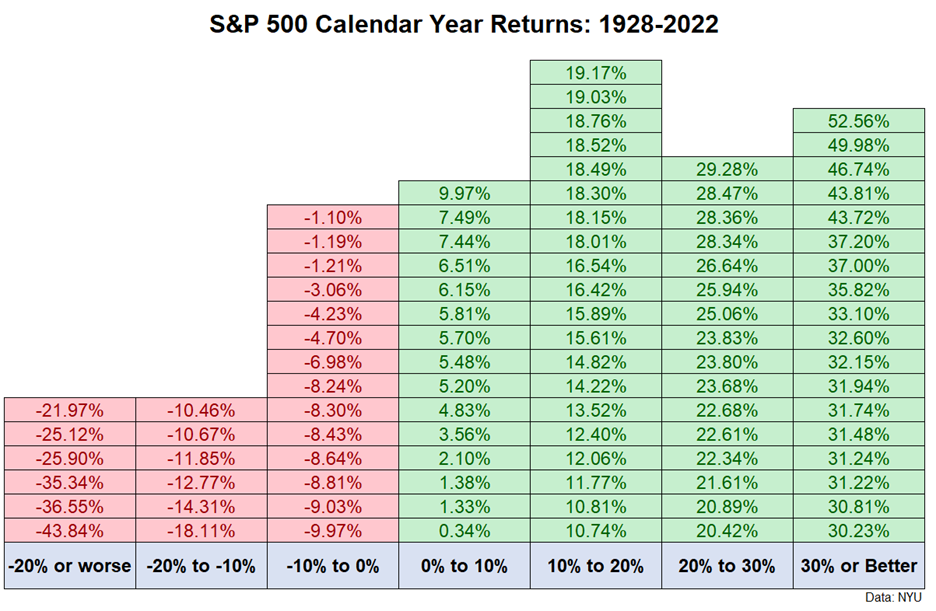

The irony is that market returns almost never come anywhere close to long-term averages in a given calendar year. In fact, the total return of the S&P 500 has only landed between 8-10% in a calendar year once (1993) since 1928.

Source: A Wealth of Common Sense

The challenge with short-term predictions is that actual short-term results are driven almost entirely by the unknown unknowns that no amount of analysis can consistently pinpoint. Case in point, I don’t recall reading a single investment outlook at the end of 2019 that prophesied a global pandemic that would upend our lives for years. Nor did any of the outlooks I perused at the end of 2021 anticipate that the Fed would hike rates further and faster than any time in modern history.

As much as I don’t care for the annual tradition of market outlooks, I would hate to leave readers empty-handed. So, while I don’t come bearing gifts of S&P 500 price targets, 10-year Treasury yield forecasts, or “cautiously optimistic” cop-outs, I do have a playbook in mind for 2023.

I call it: Silver Linings Playbook

(No, not the movie. But great flick if you haven’t seen it.)

As investors, it’s tough to maintain discipline after undeniably frustrating years like 2022. The macro clouds that have been hovering over our heads don’t just disappear because the calendar turns, no matter how badly we want them to.

High inflation, tightening financial conditions, geopolitical strife – it’s all still there. The good news is that financial markets are now well attuned to it, and hopefully beginning to look past it.

While it may not seem like it, I believe investors have much more to be optimistic about in 2023 – slowing inflation, higher yields in fixed income, more choice in portfolio diversification, less speculation, and an end in sight to the Fed’s rate hiking cycle.

Amid all the clouds, silver linings have emerged.

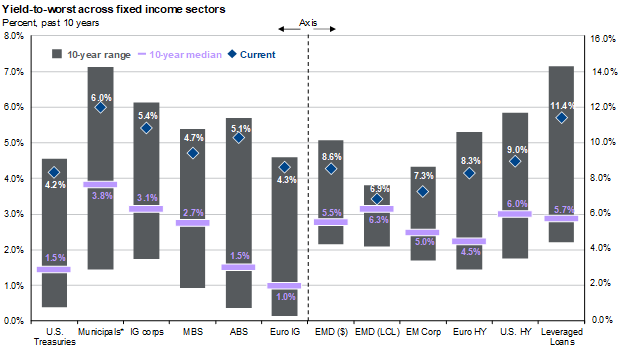

The Income is Back in Fixed Income

Prior to 2022, one of investors’ biggest gripes was the lack of meaningful yield in fixed income.

As painful as it was to get here, the good news is yield is back and bonds are poised to start behaving like bonds again.

Across the spectrum of fixed income, from U.S. Treasuries to High Yield Corporate Bonds, yields are as high as they have been in years.

Source: J.P. Morgan “Guide to the Markets”. Data as of 12/31/2022.

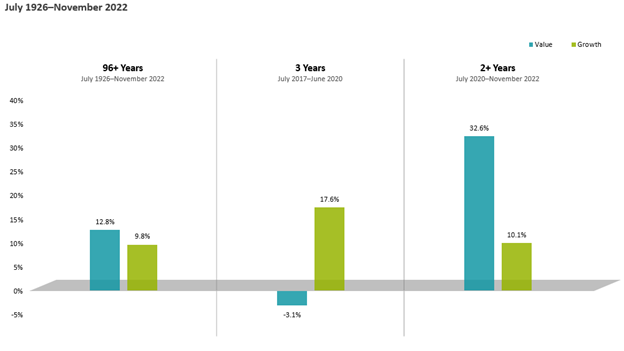

Speculation is Out, Fundamentals are In

There weren’t a lot of places to hide last year, but what was punished the most severely were the corners of the market that most benefitted from zero-interest rate policy and unfettered access to cheap capital.

Crypto fell off a cliff, the IPO and SPAC markets seized up, unprofitable tech stocks trading at nosebleed valuations were bludgeoned, and venture-backed startups found themselves in an entirely new fundraising market.

Meanwhile, investors once again began paying attention to the price they pay and the profits they expect to receive now, not in 20 years. What this has meant is that value investing –declared dead by many in 2020 – is once again en vogue.

History favors value overgrowth. But as we saw from 2017-2020, value can occasionally go out of favor in spectacular fashion. Those that maintained their conviction when the easy thing to do was give up are now reaping the rewards of their discipline.

Source: Dimensional Fund Advisors

Alternatives Earned Their Keep

While there weren’t a lot of places to hide, there were some.

It’s hard to generalize about alternative investments because it is such a heterogenous group of asset classes and strategies, many unrelated to one another.

But there were several alternatives that shined in 2022, providing diversification exactly when it was needed most.

Strategies that weathered the storm relatively well likely shared one or more of the following traits:

- Floating, rather than fixed, rates (Direct Lending, Reinsurance)

- Uncorrelated risk premiums (Reinsurance, Trend Following)

- Positive sensitivity to inflation (Trend Following, Real Assets)

- The ability to invest long and short (Event Driven, Trend Following)

Good Usually Follows Bad

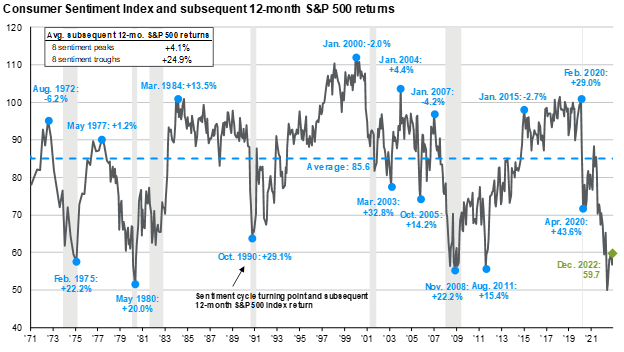

Without overstating the obvious, people don’t feel great right now about the economy. That is evident in the Consumer Sentiment index that, while off the lows, is still historically depressed.

The silver lining? Sentiment troughs are usually followed by better than average stock market returns in the ensuing twelve months. Excessive pessimism can be a source of optimism for investors.

Source: J.P. Morgan “Guide to the Markets”. Data as of 12/31/2022.

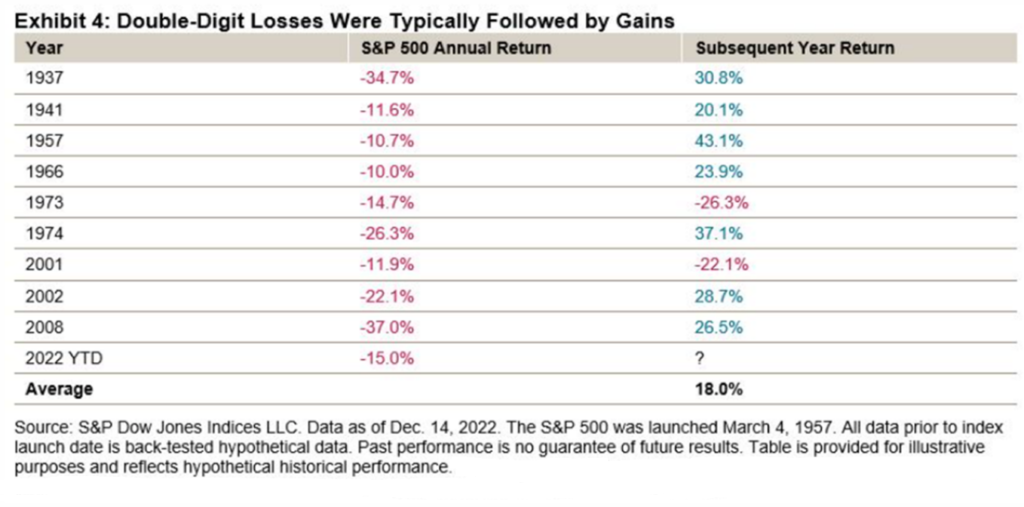

Another way of turning a negative into a positive is examining how the market has done in the subsequent year following years with double-digit losses. Of course, there are a couple of notable exceptions – nothing is guaranteed after all. But bad years have historically been followed by strong years, on average.

Please see additional performance disclosures for more information regarding the inherent limitations associated with back-tested performance.

We often place too much emphasis on one year ending and another beginning. The turn of the calendar need not precipitate a complete turnover of your life or your portfolio. Incremental improvement should be a continuous exercise.

That doesn’t mean there is never a reason to give your portfolio a fresh look – especially if it is one that has been cobbled together in a slapdash manner without a sound theoretical and empirical foundation supporting it. But for evidence-based investors, we must remember that portfolios are going to occasionally have bad years.

New Year’s Resolutions almost never work. Conversely, small incremental changes can create sustainable habits that lead to dramatic improvement in results over time. Investing is no different. Instead of poring over short-term investment outlooks, we’re much better off focusing on what we can control, biasing ourselves towards optimism, and tilting the long-term odds in our favor.

That is the ultimate playbook – and we think it will work just as well in 2033 and 2043 as it will in 2023!

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. You should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from Savant.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices or categories.