Hit a Home Run with Tax-Efficient Investment Strategies

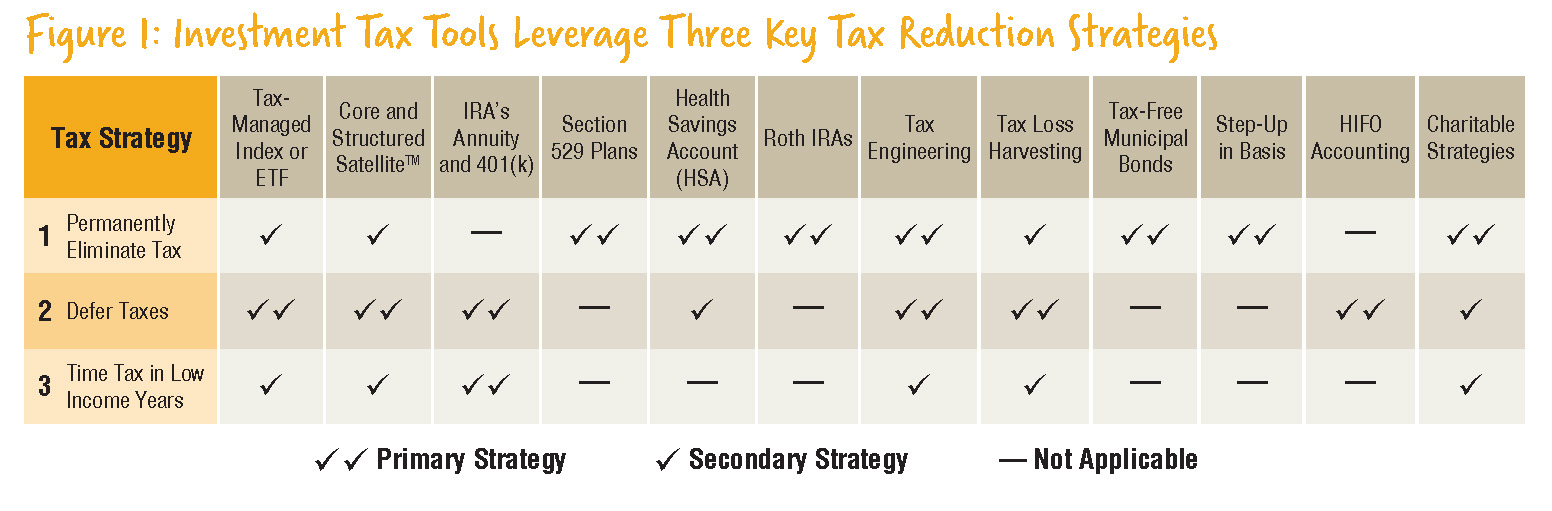

With the new tax reform, now is a good time to re-evaluate your current and future tax strategies. With the ultimate goal of increasing after-tax return, the focus here will be less on items like standard deductions, personal exemptions or child tax credits and more on investment tax tools (see Figure 1 below) that can be used to form a tax-efficient investment approach.

In the spirit of the great American pastime – baseball – here are some tips to help you hit it out of the park.

Tax-Efficient Investment Strategies

1. Tax-efficient Index Mutual Funds and Exchange Traded Funds (ETF)

Funds that attempt to “beat the market” are called actively managed funds. Funds that simply try to match the performance of an index (i.e. S&P 500) are called passively managed funds. Actively managed funds usually have higher turnover and typically have higher costs than index funds or ETFs. For tax efficiency, consider using index mutual funds or ETFs.

If you have a taxable account such as an individual or joint brokerage account, consider utilizing tax-managed mutual funds that minimize tax. Tax-managed funds look to reduce embedded gain distributions that many mutual funds generate, as their goal is to minimize tax.

2. Asset Location

Think of this often-overlooked concept as “tax-engineering” your investment portfolio. There is value to holding the right investments in the most tax-efficient account, or “tax bucket” (taxable, tax-deferred/IRA, and tax-exempt/Roth). These three main buckets catch and hold your growth. The key is to understand how, when and at what rates your investments are taxed. For example, investments with the highest long-term return prospects should be located inside a tax-exempt bucket, like a Roth IRA. Having multiple tax buckets in your portfolio also allows you to have options when and where cash needs are required in the future.

3. Tax-Loss Harvesting

The investment world offers taxable investors a consolation prize when recognizing capital losses. Tax-loss harvesting allows us to recapture some of the loss from Uncle Sam. Investors have the ability to control the timing and recognition of gains and losses. A taxpayer can use capital losses to offset current or future capital gains.

4. Specialty Tax-advantaged Accounts and Strategies

Just like a relief pitcher, designated hitter or a late-inning defensive specialist, it is beneficial to know about a variety of other potential tax-advantaged options that may come into play depending on your situation.

- Qualified Tuition or 529 Plans – Tax-advantaged savings plans are typically sponsored by an individual state and are available to help fund a beneficiary’s future qualified higher education expenses. Many states offer a tax deduction for contributions made by residents to that state’s plan.

- Health Savings Accounts – These savings/investment vehicles allow individuals and families with high-deductible health plans to set aside funds for health care expenses on a pre-tax basis.

- Gifting – Explore tax-efficient charitable gifting strategies like Donor Advised Funds and Qualified Charitable Distributions with your trusted financial professional. Their benefits vary with your tax rate, charitable intent and estate planning needs.

Like picking the perfect starting lineup, investment decision-making in light of tax consequences is both an art and a science. While many tax management techniques are small, collectively they can add up to real value. Consider these strategies to help create your run for the championship!

Tax-Efficient Investment Strategies: Key Points to Remember

- Be open to tax education

- Active management is inherently tax-nasty

- Avoid gimmicky tax-advantaged products

- Tax laws are continually changing

- Evaluate your portfolio as a whole

- Proper asset location = tax efficiency

- Harvest losses

- Be wary of outdated beliefs

- Weigh tax benefits against marginal risk/cost

- Only after-tax returns matter

Originally Published in The Voice, a publication by the Rockford Chamber of Commerce, May 2018

This is intended for educational purposes only and should not be construed as tax or investment advice. Please consult your tax and investment professionals regarding your specific circumstances.

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP® and CERTIFIED FINANCIAL PLANNER™ in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

Matthew D. Armstrong

Financial Advisor

CFP®, AIF®, CRPS®

Matthew D. Armstrong

Financial Advisor

CFP®, AIF®, CRPS®