The Factor Zoo

WELCOME TO THE FACTOR ZOO! After months of social distancing, we appreciate you venturing out for a visit to check out our exhibits. Explore the return premium to our factors: some are big, some are small and you might just find that some factors actually don’t exist at all. Over the past 60 years, you see, we’ve housed all the factors – from A to Z. As you make your way past those that did not withstand the test of time, let me tell you about a few favorites of mine.

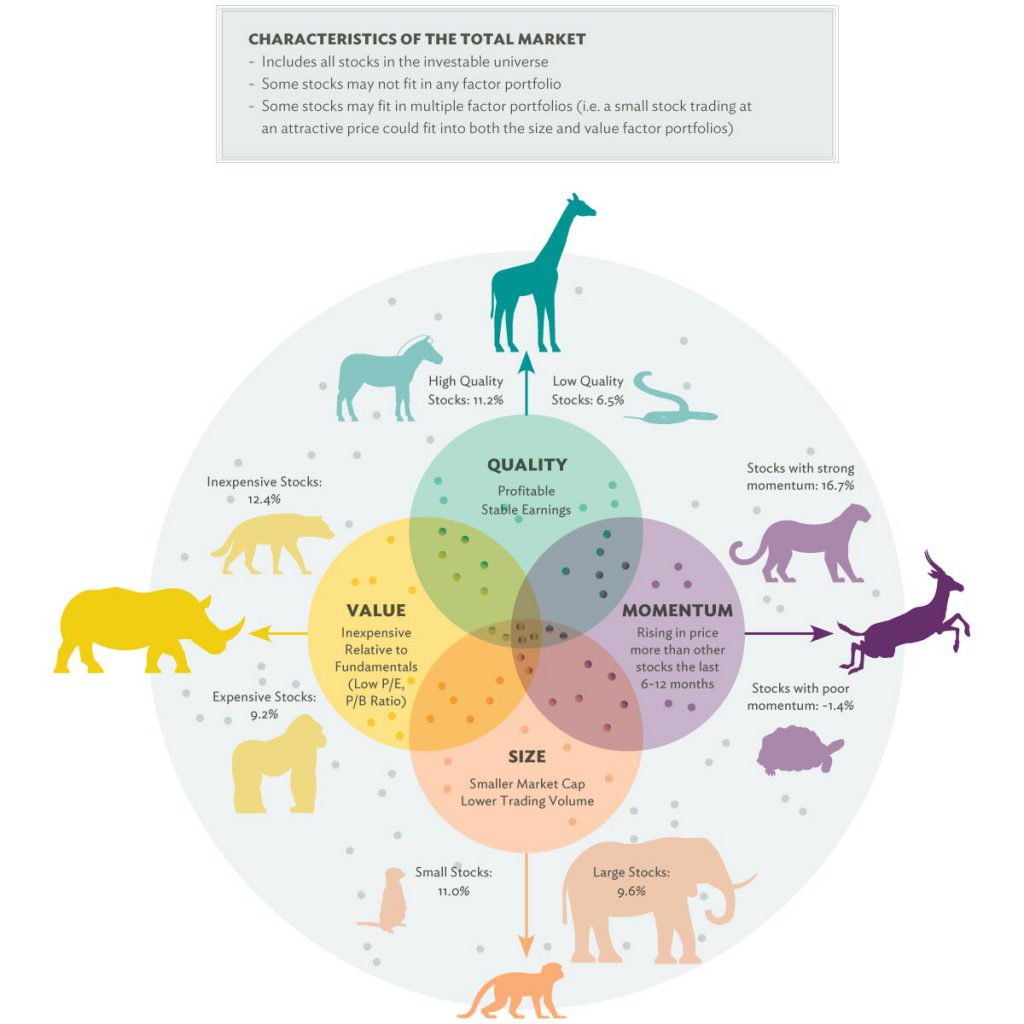

We have seen academics and professionals alike develop theories about 525 factors since 1964. In addition to surviving from one decade to the next, factors that make the cut in our portfolios must be persistent everywhere. In addition to the market premium itself, there are four equity factors that pass our test. While researchers may uncover some “factors” through data mining, we require the evidence behind factors we favor to be pervasive, persistent, and robust throughout time and across geographies, as returns to these factors are more likely to persist into the future. While even these pervasive, persistent, and robust factors do not guarantee higher returns at all times, we believe having a positive exposure to value (stocks inexpensive relative to their fundamentals), size (smaller companies), quality (companies with healthy balance sheets), and momentum (stocks with strong recent performance) should help increase an investor’s return over longer time horizons.

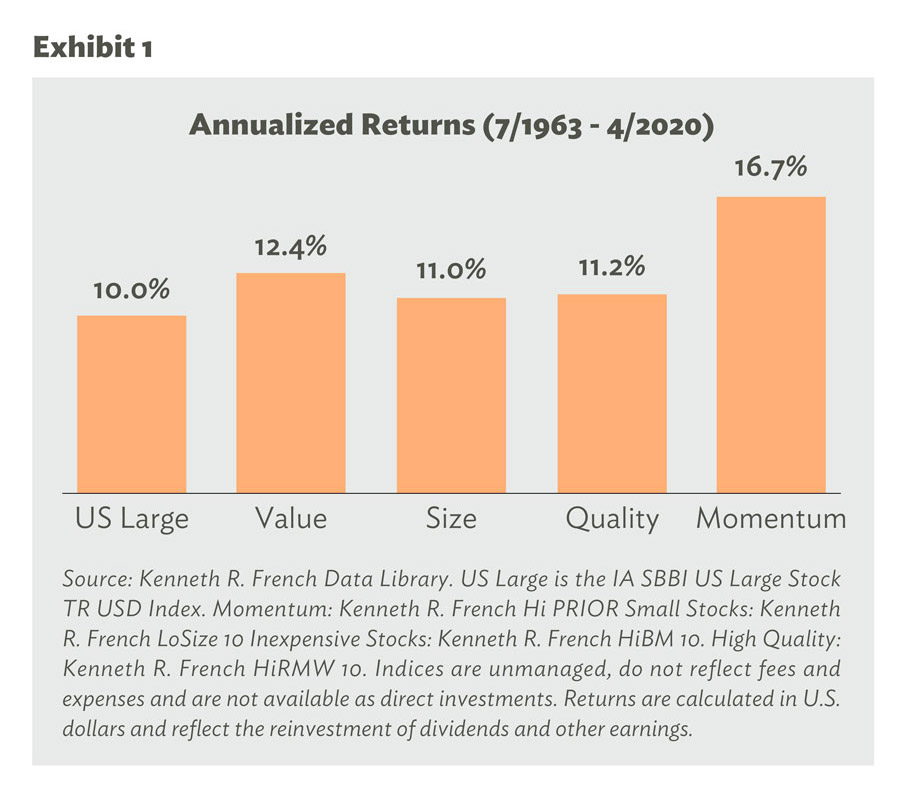

While all four of these factors have outperformed the market over the long run, each individual factor can and will suffer periodic bouts of underperformance and challenge investors’ conviction. In the late 1990s, small stocks drastically underperformed large stocks and as of late, disappointing returns from the value factor have left investors wondering if fundamentals even matter. Exhibit 1 demonstrates that each of the factors have rewarded long-term investors with returns greater than the broad market. Of course, we also must take into consideration some traits that may inflate index returns beyond what investors should expect in the real world. For example, the momentum factor requires more frequent trading, and these higher trading costs likely bring the realized premium down to be more in line with the rewards offered by value, size, and quality.

Of course, underperformance relative to the broad market is painful even if we understand it is expected along the way. So what do we think is our best tool to fight off periods of underperformance? Diversification, of course!

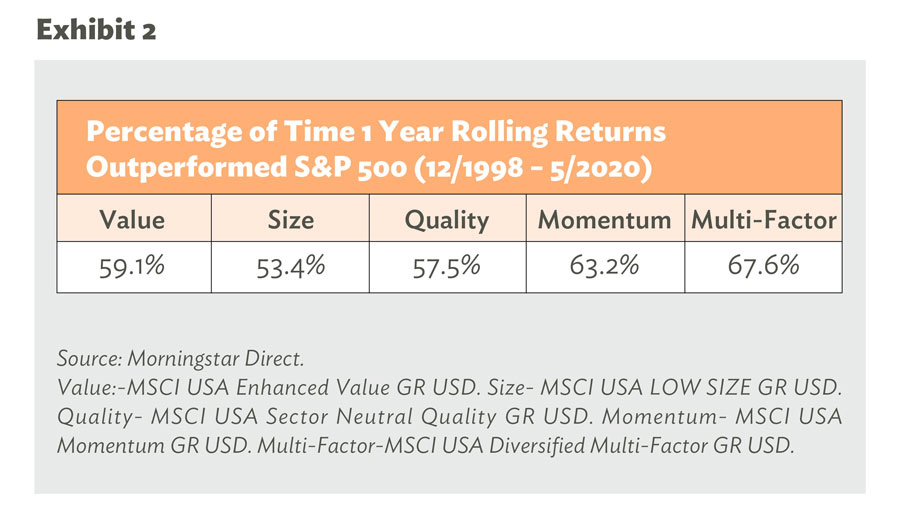

Exhibit 2 demonstrates that each factor has outperformed the S&P 500 index more often than not. But when we diversify across these factors, building a multi-factor portfolio, the consistency of that outperformance improves.

Because these factors underperform and outperform at different times, diversification can help smooth the ride for investors. Neither factor investing nor diversification is a silver bullet, meaning even multi-factor stock allocations will underperform a basic index at times. And even though the peaks of outperformance may not be as high as with a single factor, a multi-factor allocation mitigates the magnitude of underperformance as well. We believe that the evidence is robust, persistent, and pervasive in demonstrating the long-term rewards available to investors who tilt towards the value, size, quality, and momentum factors.

The Factor Zoo

Source: Kenneth R. French Data Library. All indices represent U.S. stocks and returns are from 7/1963 – 4/2020. Poor Momentum: Kenneth R. French Lo PRIOR Strong Momentum: Kenneth R. French Hi PRIOR Small Stocks: Kenneth R. French LoSize 10 Large Stocks: Kenneth R. French HiSize 10 Inexpensive Stocks: Kenneth R. French HiBM 10 Expensive Stocks: Kenneth R. French LoBM 10 Low Quality: Kenneth R. French LowRMW 10 High Quality: Kenneth R. French HiRMW 10.

Indices are unmanaged, do not reflect fees and expenses and are not available as direct investments. Returns are calculated in U.S. dollars and reflect the reinvestment of dividends and other earnings.