Tax-Loss Harvesting

The basics, the benefits, and what investors should consider

Tax-loss harvesting (TLH) can be an effective tax management tool for investors. However, a wide variety of factors can have a significant impact on the otherwise straightforward benefits of a sensible TLH strategy. Here we’ll explore how TLH works, what the expected benefits are, and what specific risks investors should consider.

What is TLH and how does it work?

TLH has gained popularity as a tax management strategy among investors in recent years. By selling investments at a loss today, investors can offset capital gains (and up to $3,000 of ordinary income) on other investments sold at a profit in the same calendar year. While TLH does not eliminate taxes altogether, the true value lies in the opportunity to lower current tax liabilities and allow for growth of those deferred tax savings over time. Consider this brief example:

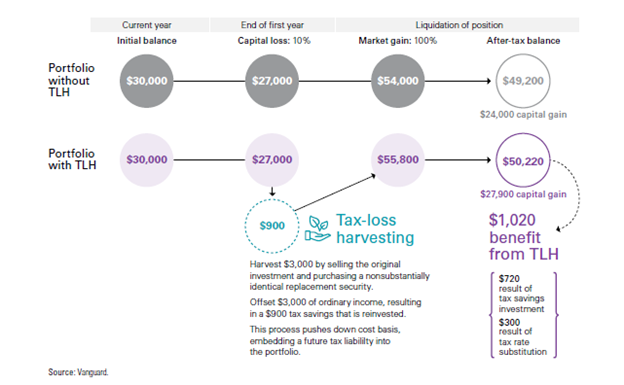

Portfolio without TLH: In the first case, we see a $30,000 investment growing to $54,000 with no transactions between purchase and liquidation. The after-tax value of this investment is $49,200 ($54,000 – capital gains tax of 20% x long-term capital gain of $24,000).

Portfolio with TLH: The second case reflects the effects of TLH. We can see that at the end of the first year, the investment has declined 10% to $27,000. The investor sells the asset at a $3,000 loss and purchases a non-substantially identical security as a replacement. The $3,000 loss offsets an equivalent amount of realized gains or taxable income that year. At a 30% income tax rate, the investor reduces their taxes by $900 that year. In this example, we assume the investor reinvests the tax savings and allows it to grow until liquidation. The result is an after-tax balance of $50,220 ($55,800 – capital gains tax of 20% x long-term capital gain of $27,900).

What are the benefits of TLH?

In our example above, TLH yielded an after-tax benefit of $1,020, originating from two components. First, the investor benefits from tax rate substitution, or tax arbitrage. By opportunistically realizing short-term losses and deferring gains, which are later realized at the 20% long-term capital gains rate rather than the 30% income tax rate, the investor creates a $300 benefit ($3,000 x 30% – 20%). Second, the investor generates an additional after-tax benefit of $720 from the growth of the $900 tax deferral, which remains invested in the portfolio and grows until liquidation.

According to several studies1, the estimated benefits of TLH range from about 0.20% to 0.85% annually. The wide range of estimates within the studies depended on the underlying assumptions around tax rates and harvesting parameters.

While TLH may provide some value to all investors with taxable assets, it can be particularly valuable to investors in higher tax brackets or investors with significant capital gains. Investors with significant assets in real estate, private equity, or private business ownership are prime candidates for TLH strategies.

What are the risks of TLH?

While the potential benefits of TLH are clear, there are several risks that must be considered. When implementing a TLH strategy, investors must weigh a variety of variables, including performance disparities between target and substitute securities, changes in tax rates and investor tax situations, and execution risk.

One of the primary hazards associated with TLH is tracking error risk during the wash sale period. Under the IRS wash sale rule, an investor cannot realize a loss on investment and purchase a “substantially identical” investment within 30 days. If violated, the realized amount is negated for tax purposes. Prudent investors will minimize the tracking error, or the performance differential between the security sold for a loss and the substitute security, while simultaneously avoiding substitute securities that trigger the wash sale rule.

At best, investors are exposed to the tracking error between the original target security and the substitute security for at least 30 days. Even short-term differences in returns between “similar assets” can cancel out the value of TLH. The substitute security may underperform the original security, rendering investors worse off. Conversely, the substitute security might meaningfully outperform the original security, or the market in general may rise dramatically over the 30-day wash sale period, creating a short-term gain. In this scenario, realizing a short-term gain to sell the substitute and re-purchase the original security may negate the original TLH benefits.

Negative tax arbitrage is also an area for careful consideration. This occurs when an investor realizes gains at a higher tax rate than when they conducted the loss harvesting. This may be the result of changes in the investor’s tax bracket over time, irregularities in the timing of other realized gains, or changes in the regulatory environment. Thus, effective harvesting should complement an investor’s financial and tax planning to avoid inefficient usage of TLH.

Execution risk refers to the actual implementation of the TLH strategy. Investors must understand a host of components underlying the TLH process to effectively execute their strategy. Important factors include what lots to harvest and at what loss thresholds. Investors should select specific tax lots with the highest cost basis, as this will generate the greatest loss per dollar of proceeds. Research suggests that a rules-based harvesting system employing a specified loss threshold can help optimize results. Selecting effective substitute securities to replace the harvested securities in the portfolio is also critical. Managing the timing of trades, specifically when to swap between target and substitute securities or vice versa, can also be daunting for individual investors.

What’s the big picture with TLH?

While TLH can be a useful tax management tool for investors, there are many factors to consider when implementing this strategy. The value of a thoughtful TLH strategy is clear, but it also comes with potential pitfalls that should be carefully considered. Investors are encouraged to examine these issues thoroughly or seek the professional guidance of qualified tax or financial planning professionals before proceeding with a TLH strategy.

Savant utilizes TLH for clients with our dedicated research and trading teams focused on proper implementation of the strategy. We have additional investment tax tools in our approach to investing in a tax-efficient manner with the goal of increasing after-tax returns. More information on this topic can be found in our white paper, Approaching Zero Taxes.

Sources:

Vanguard: Financial Planning Perspective Your mileage may vary, Setting realistic tax-loss harvesting expectations. Paradis, Khang, Dickson, 2021

Kitces: Is Capital Loss Harvesting Overvalued, 2013

Parametric: How Does Tax-Loss Harvesting Work?

WSJ: Just How Valuable Is Tax-Loss Harvesting? Dec. 4, 2021 D. Horstmeyer