ESG Investing: Does Investing for Good Impact Performance?

Did anything good come out of 2020? No doubt it was a tumultuous year as the global pandemic was accompanied by the Australian wildfires, social unrest in the United States, and corporate greed in the form of Luckin Coffee falsifying hundreds of millions in sales. According to the “Misery Index,” pioneered by economist Arthur Okun, the spring of 2020 was worse than the Great Financial Crisis and the worst period since the early 1980s when Americans faced off with high levels of inflation and unemployment. Despite a challenging year, one investing trend continued uninterrupted. According to a study by J.P. Morgan, many investors feel that the impacts of the COVID-19 crisis will further accelerate investor allocations to ESG funds.

What is ESG?

ESG is an acronym for an investment approach that takes key Environmental, Social, and Governance issues into account during the portfolio construction process. An ESG stock fund will increase allocations to companies that score well in these areas while decreasing allocations to, or eliminating entirely, companies that violate best practices. Globally, investors are utilizing ESG screens to ensure their hard-earned savings support organizations that effectively apply best practices from an environmental, social, and governance standpoint. They also want to withdraw support for companies that may harm the environment, infringe on social rights, or act irresponsibly from a corporate governance perspective.

According to Morningstar, as of January 2021, there are about 400 distinct funds domiciled in the U.S. representing an asset base nearing $100 billion that invest with an intentional ESG mandate. These ESG mandates can range from a light integration of ESG factors into security selection to more restrictive forms of impact investing that place the importance of the cause above portfolio performance. The accelerating growth in ESG investing effectively allows investors to attempt to align their investment portfolios with their personal beliefs on how corporations should act for the good of mankind.

ESG Key Issue Hierarchy

| Environmental | Social | Governance |

|---|---|---|

| Climate Change | Human Capital | Corporate Governance |

| Natural Resources | Product Liability | Corporate Behavior |

| Pollution & Waste | Stakeholder Opposition | |

| Environmental Opportunites | Social Opportunities |

But what about performance?

Very few can afford the philanthropic reach of Bill and Melinda Gates and their ability to direct billions of dollars into impactful investments while enduring minimal concern about how performance might affect their financial future (author’s note: while performance may be a secondary concern for the Gates Foundation, they certainly care about performance and monitor it closely to ensure they can continue their impactful work). For the rest of us, we may want our portfolios to positively influence organizations around the globe but cannot risk jeopardizing our financial plan in terms of performance.

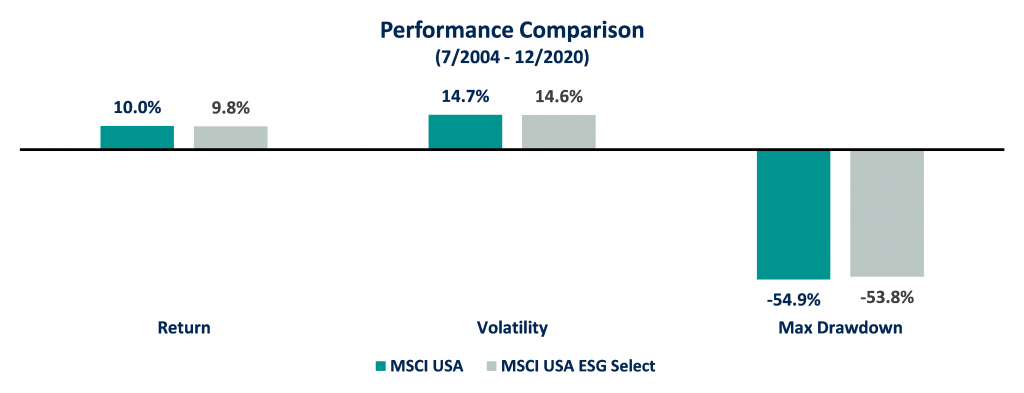

To create a meaningful comparison, we contrasted the MSCI USA Index with the MSCI USA ESG Select Index. Both indices start with the same universe of stocks (U.S. large and mid-cap), but the ESG Select Index is designed to target companies with positive environmental, social, and governance factors. This should help us to uncover any potential impacts on performance that result from companies exhibiting stronger ESG characteristics.

When it comes to performance, we must not only consider each index’s return but also the risk an investor would take to follow the strategy. Since the inception of the ESG-tilted index in 2004, it has trailed the broader universe by the slimmest of margins. From a risk perspective, there are two key metrics we can look to for insight. Volatility will demonstrate which strategy is riskier in terms of the day-to-day and month-to-month fluctuation in value. Meanwhile, max drawdown illustrates how each strategy performed during its worst stretch of performance. Perhaps unsurprisingly for believers in the efficient market hypothesis, investors in the non-ESG strategy would have experienced a marginally higher return as compensation for taking on slightly more risk through the lens of both volatility and max drawdown. Figure 1 illustrates that investors can allocate towards “good” companies and away from “bad” companies with similar performance as a broader index.

Figure 1

Sources: Morningstar Direct, Savant Wealth Analysis. Returns and volatility are annualized.

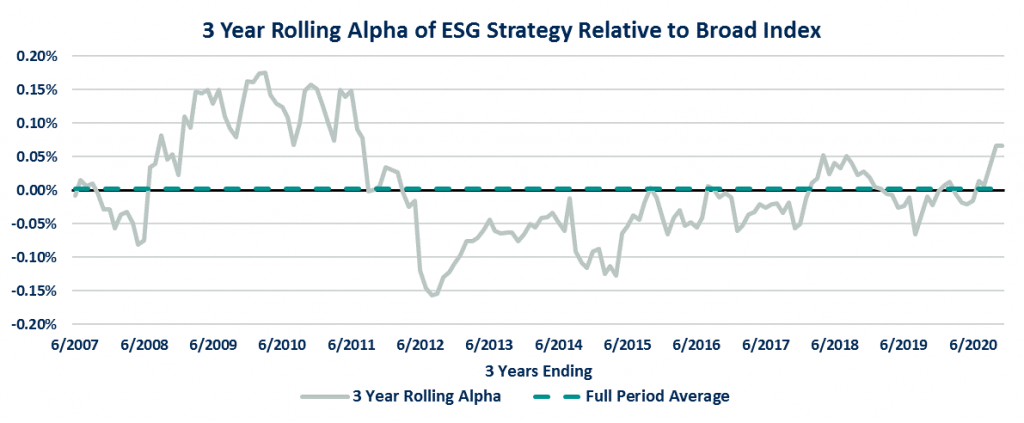

It is possible that the data appeared so close by mere coincidence. Performance of the two indices was very close over this period, but the underlying drivers of performance may create starker differences in future returns. To test this hypothesis, we can look at the three-year rolling alpha of the ESG Index relative to the broad index, complemented by a few simple risk factors. In layman’s terms, the three-year rolling alpha will tell us if differences in performance persist over time.

Figure 2

Sources: Morningstar Direct, Kenneth R. French Data Library, Savant Wealth Analysis

Figure 2 demonstrates that on occasion, the ESG strategy may perform somewhat better than the broad index when adjusted for discrepancies in the underlying risk factors. For other stretches, the ESG strategy has marginally underperformed adjusted for the same basic factors. For long-term investors, Figure 2 shows that over the full period the average rolling alpha was 0.00%, which implies that while tilting towards companies with good ESG characteristics did not improve performance, it also did not detract from performance for long-term investors. In combination, Figures 1 and 2 provide support for the argument that investors who wish to tilt towards ESG factors may be able to do so without sacrificing performance if done correctly.

If Done Correctly…

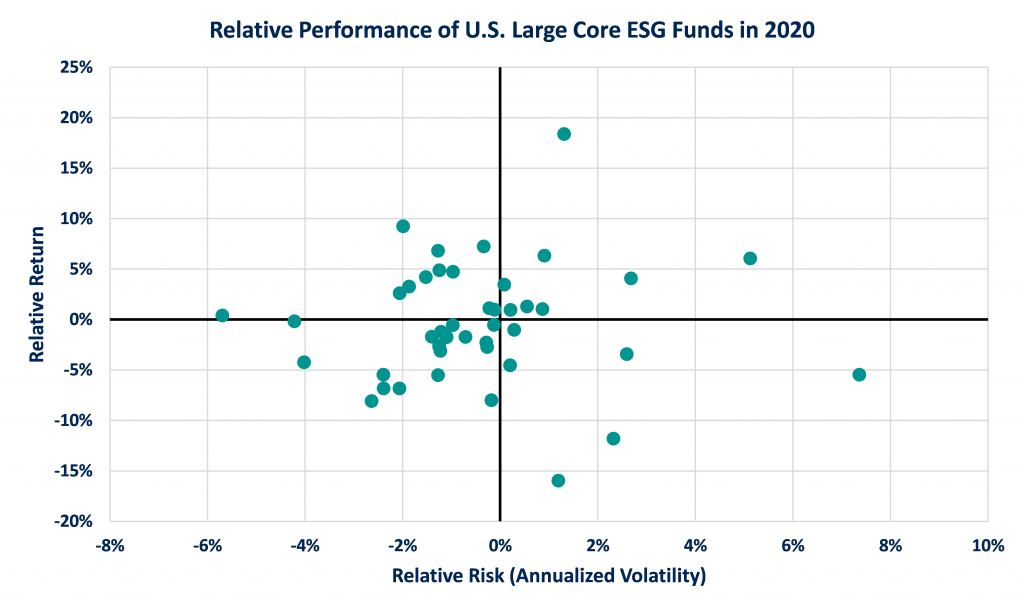

We have all seen the disclosure – index performance is historical, and indices are not directly investable. Thus far, we have compared an ESG index to a core index. But just as with standard funds, manager selection and implementation are crucial to achieving the desired risk and return tradeoff. Figure 3 aims to unveil just how well ESG fund managers were able to perform relative to the broad, non-screened MSCI USA Index in 2020.

Figure 3

Sources: Morningstar Direct, Savant Wealth Analysis

Each data point in Figure 3 represents how much more (or less) return and how much more (or less) risk each of the 44 U.S. Large Core ESG funds in the Morningstar institutional category provided relative to the MSCI USA Index in 2020. And it is all over the board! A few funds did manage a higher return with less risk than the index, but 75% of funds generated lower returns, higher risk, or worse, lower returns and higher risk. The worst offender trailed the index by over 16% in 2020 while its investors experienced more volatility.

We believe using an evidence-based investment process can help to identify which funds are more likely to fit the desired risk profile and which funds may be more likely to experience returns far different from their asset class benchmark. This evidence-based approach can help support ESG investors in their quest to allocate to good corporate citizens without sacrificing their financial plan.

ESG Investing Takeaways

In the past, many investors believed that in order to align their portfolios with personal philosophies about how corporations should act responsibly, they would have to sacrifice return, and perhaps their financial plan. However, that may no longer be the case when you consider three key points:

- An accelerating trend: Environmental, Social, Governance (ESG) investing is an accelerating trend with many more investors deciding to align their portfolios with their beliefs every year.

- Performance need not be sacrificed: For long-term investors, it may be possible to craft a portfolio with ESG funds without endangering your financial plan.

- Implementation is crucial: It has been difficult for individuals to select from a growing pool of ESG funds, as many underperformed the index in 2020. However, we believe that a disciplined, evidenced-based approach can help identify funds that are more likely to perform in line with the investor’s goals and risk profile.

This is intended for informational purposes only and should not be construed as personalized investment advice. Socially Responsible Investing has inherent limitations. Please discuss with your financial advisor to determine if this approach is appropriate for your unique situation.