Financial Planning 101

For those in the early stages of their path to financial freedom

It is essential to have a plan for the things in life that matter most. Many people believe financial freedom is important enough to warrant a plan, but unfortunately, not enough people take the time to get help or develop one. Our hope here is to help build a framework for those in the early planning stages.

Let’s start with goals that would be fantastic to achieve before retirement:

- No consumer debt

- An investment portfolio sufficient in size and structure to meet your income needs for the remainder of your lifetime

Although this may sound like a far-fetched dream to many, these goals may be feasible, depending on income, spending habits, market conditions, and other factors. Like any big goal, breaking it down into small, manageable steps will help show you that this is not only achievable, but that the process can also be enjoyable.

Let’s start with the three things that matter most when pursuing financial freedom:

- Live below your means

- Avoid debt

- Embrace the power of compound interest

The plan below assumes you are early in your career and do not have significant debt. If you are overwhelmed by debt, you should make addressing it a priority. You may need to start with a Dave Ramsey Financial Peace University class, where you can learn to eliminate debt with “gazelle intensity” using his “debt snowball” technique.

1. Live Below Your Means

The single most important step toward financial freedom is to live below your means, also known as spending less than you earn or paying yourself first.

Mastering this first step will set the course for financial independence. Regardless of income, it is a good practice to replace instant gratification with delayed gratification and to learn to live on at most 80% of what you earn without taking on debt. People at every income level have mastered this approach, and many have failed. Income level does not determine success.

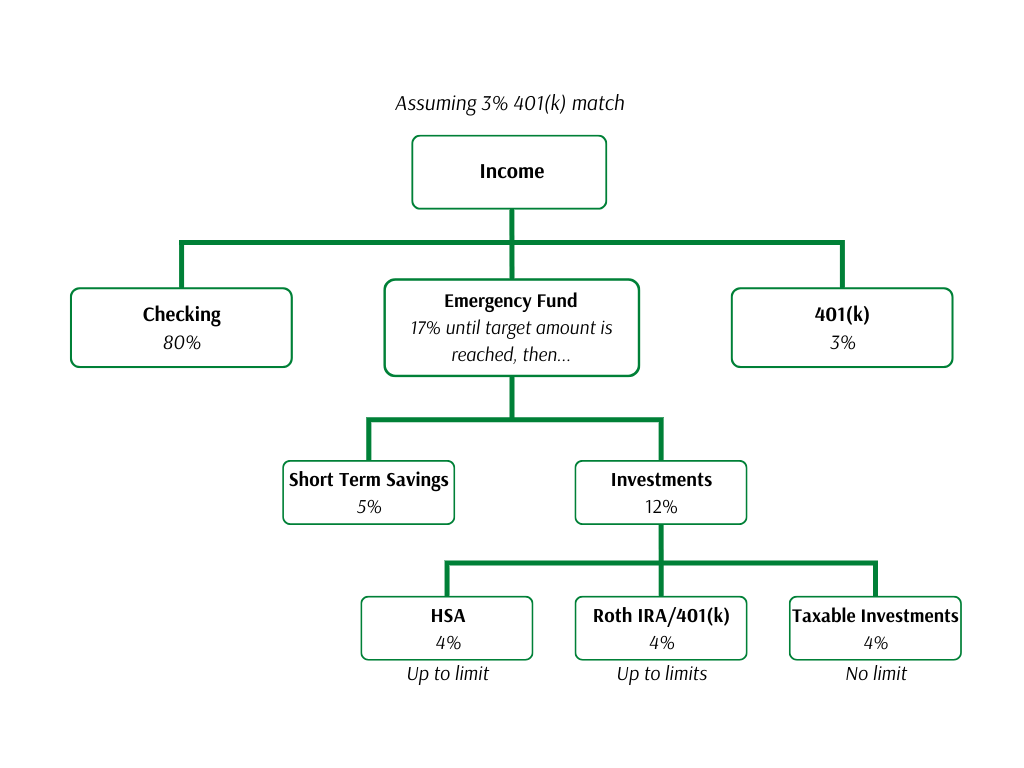

Introducing The 15/5 Savings Plan

The 15/5 Savings Plan focuses on saving 15% of income for retirement and 5% for short-term savings, for a total of 20%. Below is a suggested order for saving and investing that 20% of your income:

- Invest in your 401(k) plan, or equivalent, up to the amount of any company match.

- Emergency fund: Contribute until you reach an appropriate balance. Without a detailed calculation, six months of living expenses is a solid target. A smaller amount, such as three months, may be reasonable when you’re young, as long as you regularly evaluate and increase it over time. Hold this fund in a money market savings account.

- Short-term savings: After you fully fund your emergency account, continue saving 5% of your income to pay cash for major purchases such as a car or home down payment. Keep this fund in a money market account. You may combine it with your emergency fund as long as you maintain a minimum “emergency fund” balance.

- After you fund your emergency account and set aside 5% for short-term savings, split the remaining portion of your 20% evenly into the following buckets:

- Health savings account: the most tax-advantaged “bucket” available

- Roth IRA or Roth 401(k)

- Taxable investment account

- If or when you reach the maximum contribution for your HSA and Roth IRA or Roth 401(k), redirect those dollars to the remaining bucket or buckets. If you are a super-saver or have a high income, taxable investment accounts have no contribution limits, so continue funding them.

Here’s an example based on $50,000 of annual income:

- 401(k): 3% of income, or $1,500

- Emergency fund: 17% or $8,500, until you reach the target

After you reach the emergency fund target, the allocation would look like this:

- 401(k): 3% of income, or $1,500

- Short-term savings: 5%, or $2,500

- Health savings account (HSA)*: (12% divided by 3) equals 4%, or $2,000 (make sure you invest this account)

- Roth IRA or 401(k): 4%, or $2,000

- Taxable investment account**: 4%, or $2,000

*If you do not have an HSA, split the money evenly between the other two buckets. That equals 6%, or $3,000, into each account.

**A taxable investment account is a non-IRA investment account.

Developing the discipline to follow this plan may help improve your overall financial position, but controlled flexibility also matters. For example, early in your career, you may choose to save more than 20% while delaying some buckets as you build a 20% down payment for a home. Always make it a priority to take full advantage of any employer match.

2. Avoid Consumer Debt

Americans rely too heavily on debt to support lifestyles beyond their income levels. At first glance, this approach can appear to work until a setback changes everything. When income drops while debt remains high, personal finances can quickly unravel. Even without an income interruption, living debt-free plays a key role in achieving financial independence.

Some people view a debt-free lifestyle as nearly impossible, but if you save and gradually work your way up to bigger, better, and newer purchases, the journey can be rewarding.

Paying cash for cars, boats, and expensive vacations forces you to think carefully before making a purchase. You may decide that driving a brand-new $50,000 car is less appealing than keeping $25,000 in the bank and driving a quality used car that costs $25,000. People who avoid borrowing tend to make more thoughtful decisions about large purchases.

If you currently have a car payment, continue making that payment into your short-term savings account after you pay off the vehicle. You may need to buy a less expensive or slightly older car next time, but you will own it outright and eliminate the monthly payment.

One important note: Even if you choose a debt-free lifestyle, you will likely need a mortgage at some point. To qualify, lenders typically require an established credit history, which may require advance planning.

3. Embrace the Power of Compound Interest

Albert Einstein reportedly called compound interest the eighth wonder of the world. This money-earned-money effect only works when you invest. The most effective way to do this is by investing in the stock market.

Below is a simple approach to investing in the stock market. This portfolio may lack sophistication, but it can help you get started and is provided solely as an illustrative example. Choose low-cost index mutual funds.

70% total market index fund

30% total international index fund

This allocation may not be suitable for all investors and does not account for individual risk tolerance, investment objectives, time horizon, or financial circumstances.

That’s it. Two mutual funds can provide exposure to thousands of companies and reduce the risks associated with under-diversification. Later in your career, adding a bond index fund may help reduce portfolio volatility in some market environments.

To fully benefit from compound interest, stay invested during both strong and weak markets as part of a long-term strategy aligned with your risk tolerance, and continue contributing consistently. When markets decline, asset prices may decline.

Implementation

A plan without action amounts to wishful thinking. Automating your savings and investment strategy often provides the best chance of long-term success. Contributing to a 401(k) through payroll deduction is a common example. The key is to contribute enough and direct funds to the appropriate investment accounts.

One general approach some people consider is directing no more than 80% of your income into your checking account for everyday expenses. Many employers allow you to split paychecks between accounts. Direct the remaining 20%, or 20% minus your 401(k) contributions, into a separate savings account. From there, automate transfers into your investment accounts. Divide your annual target by 12 and schedule monthly contributions.

You don’t need to work with a broker to open investment accounts, though some individuals may benefit from professional guidance. You can open accounts directly with firms such as Schwab or Fidelity, which typically guide you through the process online.

Additional Tips

Avoid 401(k) loans. Borrowing from a 401(k) or equivalent is expensive. You borrow pretax dollars and repay the loan with after-tax dollars. When you withdraw the funds in retirement, you pay taxes again. Double taxation is never good.

Never carry a balance on a credit card. Pay the full balance on time each month.

Avoid trying to keep up with the spending habits of friends who may live beyond their means. Some may rely on debt to support their lifestyle. Surrounding yourself with financially disciplined people can positively influence your own habits.

Be cautious of financial salespeople. Many promote high-fee active mutual funds, insurance-based investments, annuities, or trading programs, which may or may not be appropriate, depending on an investor’s goals and overall financial plan.

Monitor subscription payments closely. While automating saving can help build wealth, automatic spending can quietly erode it. Review subscriptions regularly and cancel those you no longer need.

Do not gamble. Avoid online betting, casinos, and lottery tickets. The odds don’t favor you, and attempts to recover losses or strike it rich have harmed many people financially.

Use windfalls thoughtfully. At some point, you may receive a bonus, inheritance, or large gift. One possible approach is to allocate 10% for enjoyment, 30% to reduce debt, 30% toward long-term investments, and 30% for short-term savings.

Watch for lifestyle creep. When you receive a raise, consider living on two-thirds of the increase and saving or investing the remaining third. Managing your marginal propensity to consume early can help keep spending aligned with earnings.

There you have it: Financial Planning 101. While no plan fits everyone perfectly, these core principles can benefit people at any age or income level. Don’t delay getting started. If you feel behind today, acting now may help improve your financial habits over time.Top of Form

This is intended for informational purposes only. You should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from Savant. Please consult your investment professional regarding your unique situation.

Kenneth R. Duetsch

Managing Partner / Financial Advisor

CFP®, CFA®, MBA

Kenneth R. Duetsch

Managing Partner / Financial Advisor

CFP®, CFA®, MBA