RSU Checklist for Publicly Traded Companies

Following a checklist is a great way to make sure you get the most out of your restricted stock units (RSUs), manage them effectively, and avoid common mistakes. If you work at a publicly traded company, you can utilize the following list that includes best practices commonly discussed with clients, depending on individual circumstances.

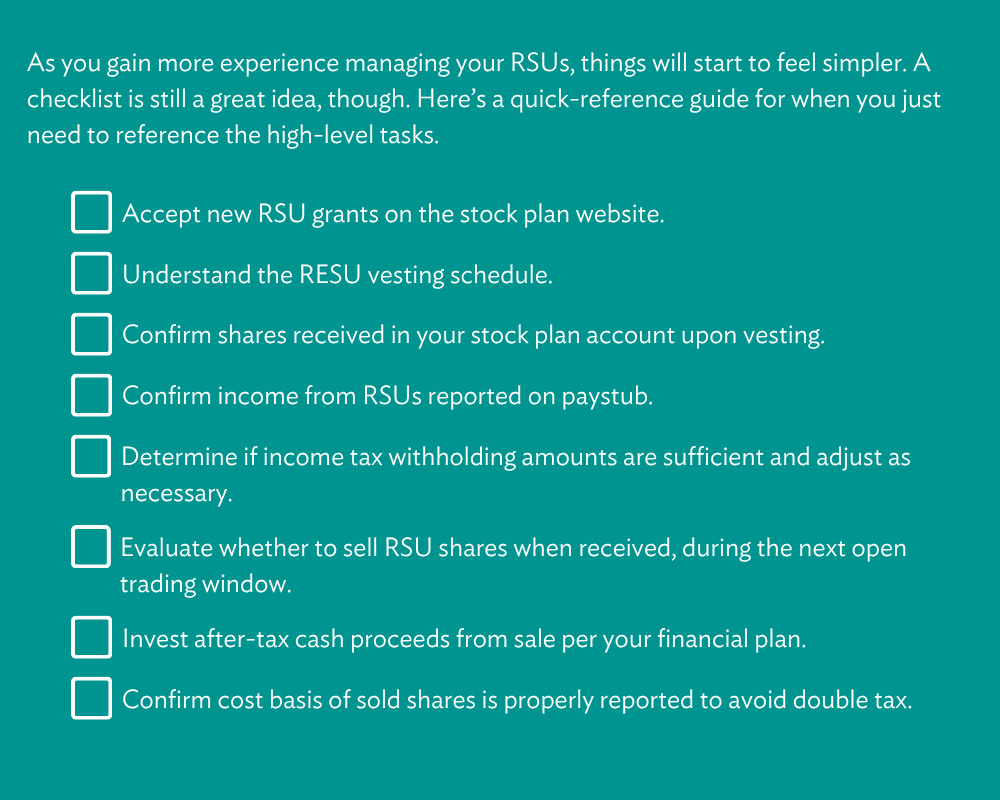

[___] Accept your grants on the company’s stock plan website when you receive them. This configures how income tax will be withheld on the value of the shares you receive.

[___] Make sure you understand the vesting schedule for your RSUs. Each new grant of RSUs has a separate schedule that specifies when you will start receiving shares, how often you will receive shares, how many shares you will receive each time, and how long you will continue to receive shares.

[___] Confirm you received the correct number of shares in the stock plan account the company has set up for you at a brokerage firm. Continue to check this periodically going forward.

[___] Confirm your paystub shows income from RSUs. The amount of income should be equal to the number of shares that vested in that pay period times the price of the shares when they vested. Continue to check this periodically going forward.

(Note that there may be a confusing line item on your paystub labeled “RSU Offset,” “Stock Offset,” or something similar. You can ignore this. This line item has to do with the fact that income on RSUs is non-cash income, and an adjustment must be made on your paystub to show you did not receive cash for the income represented by the shares you received.)

[___] Determine if the income tax withholdings on your RSU income will be sufficient to cover the amount of tax you will owe. Remember, when RSUs vest, the value of the shares you receive are taxed as ordinary income at your regular income tax rate (not the lower long-term capital gains tax rate). Be sure to set your income tax withholdings to cover your full tax obligation. Many companies withhold federal income tax on RSUs at a rate of 22%, which may be too low for your situation.

[___] Consider whether to sell your vested RSU shares when permitted under your company’s trading windows and policies. You may need to wait until your company’s next open stock trading window. There will generally be no additional tax owed if you sell right away, and there is often no tax benefit to holding your shares. The decision to sell is purely an investment decision, and diversifying your investments by selling your RSU shares can help reduce concentration risk for some individuals.

[___] Distribute and invest the cash from the sale of RSU shares according to your financial plan. Some general considerations that may apply depending on your circumstances: Be sure to first set aside any extra cash needed to cover income taxes if your withholdings are too low. If you have credit card debt, student loans, or other consumer debt at high interest rates, consider paying down those loans next before investing. Then direct cash as needed toward near-term savings goals, such as a down payment for a home. Finally, invest the remaining cash toward long-term goals, such as education savings or retirement.

[___] When you receive your tax reporting documents after year-end, confirm that the cost basis of RSU shares you sold during the year is properly reported on IRS Form 1099-B. There should be a value other than $0 in box 1e on Form 1099-B. If box 1e does contain a value of $0, you may inadvertently pay tax twice on the RSU shares you sold during the year.

Using the checklist regularly can help reduce mistakes and support more informed financial decision-making over time.

For more information on RSUs, including the pros and cons of selling shares right away when you receive them and how to avoid paying tax twice on sales, see these articles:

An Introduction to Restricted Stock and RSUs

When Should You Sell RSU Shares?

Cashing Out RSUs: Dodging Tech Stock Disasters by Diversifying

Bruce R. Barton

Managing Partner / Financial Advisor

CFP®, CFA®, MBA

Bruce R. Barton

Managing Partner / Financial Advisor

CFP®, CFA®, MBA