Divorce Help: Financial Planning and How to Regain Your Confidence

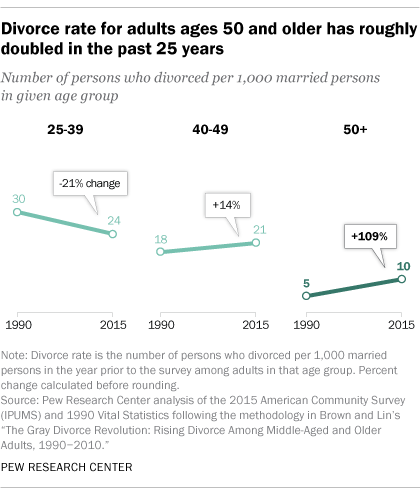

While divorce has long been associated with younger couples navigating the challenges of early marriages, a new pattern is emerging where couples are deciding to end their unions later in life. Research shows divorces involving couples 50 and older have more than doubled since the 1990s. Looking further, the divorce rate among couples aged 65 and older has more than tripled.

The hardest group hit? Those divorcing from a second or third marriage.

This shift highlights the growing need for thoughtful divorce financial planning, especially for individuals navigating complex financial transitions later in life.

Just like any divorce, gray divorce happens for many reasons, but one of the primary reasons is evaluating the opportunity for happiness in the future. As responsibilities change, children become more independent and no longer need as much care. This can create more freedom to focus on what each partner wants in the years ahead, making financial planning an important step in preparing for this transition.

Finances can also strain a marriage, especially if one spouse favors saving while the other spends more. While separating may help reduce that tension, financial planning after divorce is essential to help ensure long-term stability and independence.

If you find yourself going through or recovering from a gray divorce, how do you determine what steps to take next financially after divorce?

Post Divorce Checklist

Divorced at last? After you finalize your divorce, there is still much to do. Savant’s Post-Divorce Checklist serves as a helpful financial resource for post-divorce financial planning and is provided for general informational purposes only.

Rethink Your Financial Priorities

For your first step in divorce planning, reflect on your financial priorities for the future.

As a couple, you likely had goals and objectives you created together. However, divorce is a significant life transition. After you are no longer married, you can create a new life on your own terms.

Take the time to think about what is important to you going forward. You may pursue new and different goals or better align your former goals with your future priorities. This clarity can help you decide how to alter your spending and financial priorities.

Revisit Recurring and Regular Expenses

When you’re single again, it can be a shock to manage all monthly expenses alone. It’s possible, but it requires attention to your spending as you work through your changing situation.

Think about what you can continue to prioritize with your finances and what may have to change. Are you keeping the house? Does it still have a mortgage? You’ll need to include the mortgage payment in your budget. Besides the mortgage, there are property taxes, insurance, and home maintenance to cover.

Next, you may need to think about alimony when seeking divorce help. In many long-term marriages, divorce can result in extended or even ongoing alimony obligations. Shorter marriages might involve shorter-term payments. Alimony payments may be welcome income for the recipient and a financial burden for the payer, with tax rules now limiting deductions and tax liability shifts.

If you expect to pay alimony, it’s important to consider how those payments will affect your overall budget.

What other regular expenses will you incur? Consider the cost of your daily living expenses and any outstanding debts or obligations, including:

- Health care expenses, both insurance costs and ongoing cost of care for medical needs. You may not yet be eligible for Medicare, and if you are, it’s important to assess whether the coverage meets your needs or if a supplemental policy may be necessary.

- Financial support you provided or promised to children or grandchildren.

- Ongoing payments for country club or HOA membership dues.

- Yard and lawn care, housekeeping, utilities, cable, or other needs.

- Regular insurance payments, such as life, auto, or long-term care.

- Subscription costs, whether to periodicals, regular deliveries, streaming services, audio or book databases, etc.

- Travel commitments, vacation homes or leisure items, or timeshares.

As you review expenses, this is where it pays to think things through.

There may be ways to help you reduce ongoing expenses. You could consider downsizing your current home if the expenses for upkeep are too significant. If you own a second home, it may make sense to consider selling one residence. If you own a luxury vehicle, you could consider driving a car with a lower purchase price and maintenance costs. These changes may add liquidity to your personal finances, which can help assist with ongoing living expenses.

Consider the costs of “extra” commitments such as a private dining club membership, country club access, or something as minor as a subscription service you don’t use.

Another key consideration in divorce planning is understanding your income tax liability, which can look very different when filing as a single taxpayer rather than jointly. If you are still working, you may need to revise your paycheck withholdings. If you are retired, you may need to adjust your quarterly estimated tax payments.

Also, if you’re supporting loved ones like adult children or grandchildren, you may need to revisit your ability to help. Remember, students can access college loans, but there’s no financing available for retirement savings. Be conservative with what you can offer your family until your finances are settled.

Splitting Assets in the Divorce

In a divorce settlement, each asset will be identified and clearly divided in the documentation.

While this process seems relatively straightforward, it’s an area where making smart financial choices can have an impact on the final settlement. As you are negotiating the property settlement with your spouse, it is imperative that you consult a professional who can assist you with the tax ramifications of accepting certain assets as part of this property division.

For example, in a divorce settlement agreement, one spouse can receive the entire retirement account and IRA, while the other spouse receives the personal investment accounts. While each account has the same balance, the division may not create parity. Every dollar withdrawn from a retirement account is generally taxed as ordinary income. In a personal investment account, only capital gains from investment growth and dividend income are generally taxed. In this case, the personal investing account typically generates less tax compared to an IRA or other retirement account.

Advice from a qualified financial advisor may be helpful in a divorce. The advisor needs to understand tax laws and evaluate a property and assets settlement not only in terms of total dollars, but also single-taxpayer status and income. They can help you assess how different assets may fit within your financial plan once the divorce is final.

Before the final decree, it’s wise to look ahead and estimate. Compare your potential share of the assets to your liabilities and project where that leaves your financial situation. Will you need to supplement with part-time income or withdraw more money from your retirement accounts to get by?

As you divide the assets, it’s essential to update the beneficiaries for each asset that requires a designation. Reviewing and updating the beneficiary on each account helps protect your legacy and can reduce the risk of assets going to a former spouse.

Review Possible Adjustments to Your Investments

Now that you’re single, you may have different investment priorities and risk tolerance, which will likely affect your investment portfolio’s allocation.

For example, if you lost part of your retirement account balance or income stream from the divorce, you’ll need to determine how to proceed. You could take more risk to potentially increase your return, but that can also increase the chance of loss.

Instead, you can consider engaging a financial advisor who also provides tax-focused planning to help maximize your tax efficiency. Their goal is to help you evaluate tax-efficient planning strategies based on your individual circumstances.

Update Your Insurance Policies

You’ll probably need to update the beneficiaries on your insurance policies.

This is also an excellent time to consider reducing or increasing your coverage. Make sure your home, auto, and personal property insurance properly reflect your current situation. You may not need some of the insurance policies you had while you were married.

Legal Documentation

Along with the beneficiaries on your insurance policies, it’s important to update any legacy documents:

- Will

- Financial Power of Attorney

- Medical Power of Attorney

Often, a person will name their spouse as the executor and heir to their estate. Through a power of attorney, a former spouse may still have the right to handle your financial and health care decisions if you’re incapacitated. It’s critical to update these documents to include individuals who are more appropriate.

Health Care

If you are covered by Medicare, be aware that your premium can change based on life circumstances.

After the divorce is final, you should check your Medicare premium, which is based on the income reported on your tax return two years ago. The higher your income, the higher the premium. You were likely paying a Medicare premium rate based on your married status and income level before your divorce. Processing a ‘change in life event’ with the Social Security Administration may allow you to lower the monthly premium to better match your current income, rather than income from two years prior. Note: This change is not automatic; a financial advisor can help you review available information to determine if you may qualify for a reduced premium.

If you are still covered by your spouse’s employer-sponsored health insurance policy, you will need to find a new plan. If you’re employed, you can enroll in your employer’s health plan. If that’s not an option, you can potentially extend your coverage through COBRA or apply through the affordable care marketplace. COBRA currently allows an individual who is losing employer coverage due to divorce to keep the coverage for 36 months as compared to the typical 18-month timeline. This means you may have some time to evaluate the options and compare the costs of COBRA to an individual health care policy.

Social Security

Divorce can impact your Social Security as well. Were you married for over 10 years? If so, you may be entitled to receive Social Security benefits on your ex-spouse’s record, which may mean a higher benefit if they earned more, provided:

- You are unmarried, and

- You are 62 or older, and

- Your ex-spouse, remarried or not, is entitled to Social Security retirement or disability benefits, and

- The benefit based on your work history is less than what you would receive based on your ex-spouse’s work record.

Moving Forward After Divorce

If you’re going through a divorce, take time to take care of your health and emotional well-being. Divorce can be a draining process, but it also presents an opportunity to reset and move forward with clarity and purpose. As you rebuild your life, focusing on your goals and making thoughtful financial decisions can help you regain a sense of control and stability.

Financial Resources for Women After Divorce

Navigating the financial complexities of divorce can feel overwhelming, especially when you may be making decisions on your own for the first time. Savant’s Wife2CFO Program is designed to support women through major life transitions by providing educational resources, financial guidance, and a supportive community. From understanding your financial picture to planning for the future, these resources are intended to provide general education and framework considerations to help you move forward with greater confidence and clarity. Taking these steps can help you rebuild your finances after divorce.

Why Choose a Savant Financial Advisor After Divorce

Divorce brings significant financial changes that often require a thoughtful and coordinated approach. Working with a financial advisor can help you evaluate your assets, understand tax implications, and develop planning considerations aligned with your new financial reality. At Savant, our team works with individuals navigating life transitions to develop personalized strategies designed to support long-term financial planning objectives. Schedule an introductory call with a Savant advisor to learn how we can help you take the next step forward.

Frequently Asked Questions About Divorce Financial Planning

What should you do financially after a divorce?

After a divorce, it is important to reassess your financial priorities, review your budget, update legal and financial documents, and create a plan for managing your income, expenses, and investments moving forward.

How do you rebuild finances after divorce?

Rebuilding finances after divorce involves creating a realistic budget, managing debt, reassessing investment strategies, and setting new financial goals that align with your current situation.

What is included in a divorce financial checklist?

A divorce financial checklist typically includes reviewing assets and liabilities, updating beneficiaries, evaluating insurance coverage, adjusting tax strategies, and planning for future income needs.

How does divorce affect retirement planning?

Divorce can impact retirement planning by changing your income sources, splitting retirement accounts, and altering long-term financial goals. It is important to reassess your retirement strategy based on your new circumstances.

What services does Savant provide for divorce financial planning?

Savant provides divorce financial planning services that include evaluating assets and liabilities, analyzing tax implications, guiding investment and retirement decisions, and helping create a comprehensive financial plan tailored to your new financial situation.

Wife2CFO™ is a branded initiative of Savant Wealth Management. Investment and financial planning services are provided by Savant Wealth Management, a Registered Investment Adviser. This content is provided for informational and educational purposes only. It does not constitute legal, tax, or investment advice. Please consult qualified professionals for advice specific to your situation. Please visit wife2cfo.com for more information.