Ask Meaningful Questions: International Investing and Factor Investing

Introduction to Step Two of Evidence-Based Investing

Being leaders in the investment business also means being detectives, researchers, and educators. Individuals come to us with questions, and it is our responsibility to provide thorough and evidence-based answers that lead to successful outcomes.

Throughout our whitepaper, “Evidence-Based Investing: A Scientific Framework for the Art of Investing,” we ask and answer meaningful questions around a variety of topics. Evidence-based investing, or EBI, is the foundation of our investment philosophy. It’s designed to build globally-diversified portfolios that minimize unrewarded risks and maximize after-tax return. EBI involves a four-step process.

In step one, we concluded the conventional approach to investing adds unnecessary risk and costs. In this blog, we’ll kick off step two of the EBI process by answering meaningful questions around international and factor investing, and provide you with a preview of some of the research that is explored at more length in the whitepaper.

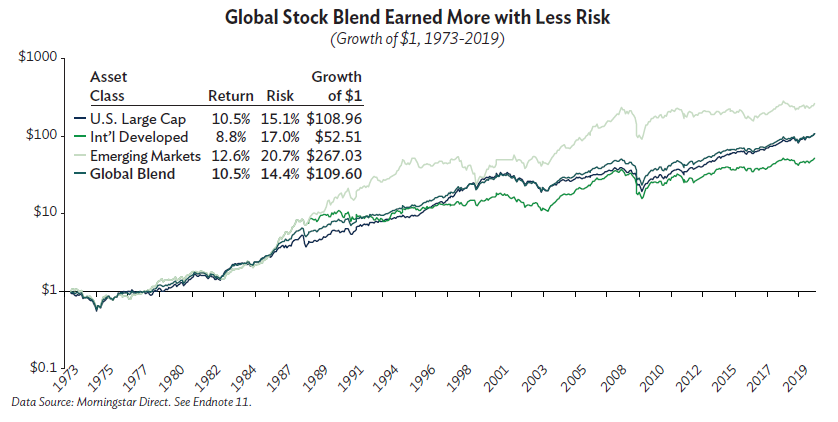

Question: Is it advantageous to diversify overseas?

Answer: The short answer is yes. The global economy has grown much larger than that of the U.S., with 76% of the world’s gross domestic product being generated outside the United States. Not considering international investing is a lost opportunity.

International stocks behave differently than U.S. stocks, a known fact supported through data. International and U.S. markets have volleyed delivery of highest returns for the past 40 years – with international taking top billing during the 1980s, the U.S. in the 1990s, and so on.

Global diversification provides access to a larger number of stocks, which broadens opportunity in key markets across developed and emerging market countries. It makes good business sense to monitor global consumption habits and invest in such companies.

Evidence: As detailed below, a blended portfolio with both U.S. and international exposure delivered a similar return with lower risk when compared to portfolios that are singularly focused – compelling evidence to include international stocks in a diversified portfolio.

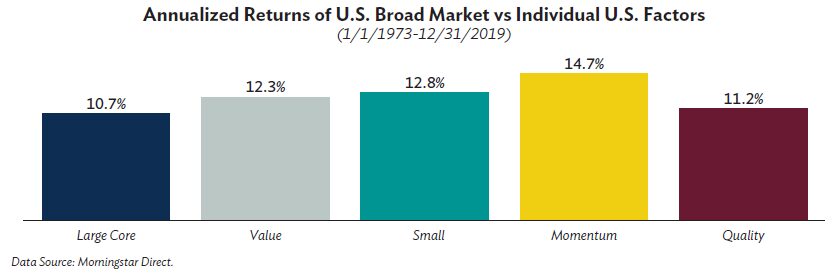

Question: Should investors overweight stocks with attributes associated with higher expected returns?

Answer: There are many factors with higher expected returns that investors can target, which are supported by academic evidence. However, only four factors, which we explore below, get the stamp of approval for inclusion in our portfolios at this time. By no means are they guaranteed to outperform every year; these four factors will still experience ups and downs. Our research shows that when used together in a portfolio, they can help deliver more consistent outperformance relative to the broad market for long-term investors.

- Size: Don’t sleep on small company stocks. Though more volatile, they comprise the largest number of stocks, and their superior returns hold true around the world (returning an average of 11.4% compared to 10.2% for U.S. large stocks and 13.5% compared to 8.7% for international large stocks over a nearly 50-year period).

- Value: Bargain stocks should never fall out of fashion. Evidence shows that value stocks have outperformed their flashier, buzzworthy relative – the growth stock – since 1975. That said, we still encourage owning value and growth, as leadership is cyclical. Resist the temptation to just value shop, as the importance of diversification still applies here.

- Quality: The phrase “quality over quantity” rings true for investing. Examples of quality metrics to consider include high return on equity, stable year-over-year earnings growth, and low financial leverage.

- Momentum: Momentum is probably the least intuitive of all factors, as it goes against the first lesson most investors are taught: buy low, sell high. But in general, stocks with the strongest recent performance tended to maintain that strong performance, while stocks with the weakest recent performance saw continued poor performance. The figure below demonstrates how momentum strategies resulted in a return premium for long-term investors who stayed the course. This factor does require more frequent trading, which brings it more in line with the other three factors.

Evidence: Research shows that size, value, quality, and momentum outperformed the broad U.S. market on a rolling 12-month basis, which means performance improves when we prioritize our diversification efforts across these four factors.

In Summary

You’ll see us continue to stress the importance of portfolio diversification, and two key strategies we use are international investing and factor investing.

Our next blog will address and delve into more meaningful questions around diversified portfolios with alternative investments.

For more information, download our EBI whitepaper or consult with your financial advisor.